The Balance of Payments

Download the complete Explainer 112KBThe balance of payments summarises the economic transactions of an economy with the rest of the world. These transactions include exports and imports of goods, services and financial assets, along with transfer payments (like foreign aid). The balance of payments is an important economic indicator for ‘open’ economies like Australia that engage in international trade because it summarises how resources flow between Australia and our trading partners.

This Explainer looks at the structure of Australia's balance of payments.

The Structure of the Balance of Payments

Australia's balance of payments captures the transactions between Australian ‘residents’ and the rest of the world, in a given period. ‘Residents’ are defined broadly to include people who live in Australia, businesses that operate in Australia, the Australian Government and other organisations that operate here.

The balance of payments divides transactions into two broad accounts:

- the current account

- the combined capital and financial account

In essence, the current account captures the net flow of money that results from Australia engaging in international trade, while the combined capital and financial accounts capture Australia's net change in ownership of assets and liabilities. These broad accounts are often referred to as the ‘two sides’ of the balance of payments.

The balance of payments are put together according to international standards (set out by the International Monetary Fund (IMF) and the United Nations) that make it easier to compare Australia's balance of payments with that in other countries.

The Current Account

The current account records the value of the flow of goods, services and income between Australian residents and the rest of the world. There are three components to the current account – the ‘trade balance’, ‘primary income balance’ and ‘secondary income balance’. In economic analysis or commentary, most attention is usually given to the trade balance, which records the difference between the value of our exports and imports of goods and services. This is because the trade balance forms part of gross domestic product (see Explainer: Economic Growth).

| Current Account | |

|---|---|

| Trade balance | The value of goods and services that Australian residents export less those that they import. |

| Primary income balance | The income that Australian residents earn from, less that they pay to, the rest of the world from working (e.g. wages) and from financial investments (e.g. dividends). |

| Secondary income balance |

Consists of two parts:

|

The term ‘current’ is used in describing the current account because the goods, services and income being traded in will be consumed or received in the current period (specifically, within the quarter).

The Capital and Financial Account

The combined capital and financial account records the capital and financial transactions between Australia and the rest of the world.

The capital account component records two main types of transactions involving capital. The first is ‘capital transfers’, where one party has transferred ownership of something to another party without receiving anything in return; capital transfers include conditional grants for specific capital projects (e.g. a foreign aid project to build roads) and forgiveness of debt. The second type of transaction involves ‘non-financial, non-produced assets’; this type of asset includes intangible assets (e.g. brand names) as well as rights to use land or water (e.g. for mining or fishing).

| Capital Account | |

|---|---|

| Capital transfers |

Transactions where one party

has transferred ownership of

something to another party

without receiving anything

specific in return. For example:

|

| Acquisition/disposal of non-produced, non-financial assets |

|

The much larger financial account component records transactions between parties that involve a change of ownership of Australia's assets or liabilities. It is structured according to the different classes of investment that owners of these assets or liabilities can undertake.

| Financial Account | |

|---|---|

| Direct investment | Financial transactions related to long-term capital investment in a business (e.g. purchase of machinery, buildings and factories), where the investor has significant – 10 per cent or more – voting power in the business (i.e. through ownership of ordinary shares or voting stock). |

| Portfolio investment | The purchase of equity or debt (shares or bonds) in a business. In contrast to direct investment, portfolio investment occurs when the investor does not have an influence in the operation of the business. |

| Financial derivative | The purchase or sale of financial derivatives (i.e. financial contracts between two parties where the value is derived from another financial instrument, such as a bond or share, or a market index). These transactions involve the exchange of risk between parties, rather than funds. |

| Reserve assets | The purchases or sale of reserve assets held by the Reserve Bank. These reserves are assets controlled by the Reserve Bank to meet policy objectives such as intervention in the foreign exchange market and to assist the Australian Government in meeting its commitments to the IMF. |

| Other investment |

Transactions that do not fit into

one of the other categories. One

example is ‘trade credit’ where an

importer purchases goods from

overseas and does not pay for

the goods until they are received. Another example is ‘currency and deposits’, where money is deposited in or withdrawn from banks across borders, or banknotes and coins are transferred between countries. |

Accounting Framework

Double Entry

Any transaction has two sides. In an economic transaction, something of economic value is provided and something of equal value is received. This notion is reflected in the ‘double entry’ accounting framework used in the balance of payments. In this framework, for every transaction between an Australian resident and the rest of the world, the balance of payments will record two entries. When economic value is provided a credit entry is made, and when an economic value is received a debit entry is made. The credit and the debit will be for the same amount, but the credit will be recorded as a positive entry and the debit will be a negative entry. For example, when a shipment of wheat is exported from Australia to an overseas buyer, a credit entry will be made in the balance of payments reflecting the value of the shipment that has been provided to the overseas buyer. On the other side of the transaction, the Australian seller receives a payment for the wheat shipment and this payment is recorded as the offsetting debit entry. Since every transaction in the balance of payments has two offsetting entries, the total balance of payments should be zero.

Net Errors and Omissions

While the total balance of payments should be zero, this does not always occur in practice. This can be due to measurement errors, because it is difficult to accurately record every single transaction between Australian residents and the rest of the world. And sometimes transactions are not measured at all – they are ‘omitted’. Because of this there is an additional item included in the balance of payments, known as ‘net errors and omissions’, to ensure that it always balances.

Box: Some Examples of Credits and Debits

To help illustrate the distinction between different economic transactions and how they are recorded in the balance of payments, consider the following examples.

-

An Australian mining company exports $100 million of iron ore to a private Chinese steel maker. The Chinese steel maker will only provide payment for the shipment once it arrives in China from Australia (which is known as a trade credit because payment is only made after the goods are received).

The $100 million shipment of iron ore from Australia is an export and is recorded as a ‘goods credit’ under the trade balance. The trade credit payment from the Chinese steel maker is recorded in the financial accounts as a debit under ‘other investment – trade credit’.

-

Australian residents, including friends Michelle and Megan, go on overseas holidays to Bali during winter and spend a total of $5 million. The Australian residents pay for their holiday by using money deposited in their Australian bank accounts.

The $5 million Australian residents spent on overseas travel is an import and is recorded as a ‘service debit’ in the trade balance (specifically ‘import – tourism’). The payments made to overseas households and businesses (for the accommodation, food, sightseeing, etc.) by the Australian residents from their domestic bank accounts are recorded in the financial accounts as a credit under ‘other investment – currency and deposits’.

-

Taylor, an Australian resident, buys $20 million of shares in a company listed on the New York Stock Exchange, equivalent to less than 10 per cent of the voting rights in that company. The shares are paid for using money from Taylor’s bank account in Australia.

The $20 million of shares purchased by Taylor is recorded in the financial account as a debit under ‘portfolio investment’, because the purchase does not result in a significant degree of influence over the firm. The payment for the shares is made from Taylor's Australian bank account and recorded in the financial accounts as a credit under ‘other investment – currency and deposits’.

| Sample of Balance of Payments* | |||

| Credit | Debit | Net (Credit plus Debit) |

|

| Current account | $100m | -$5m | $95m |

| Trade balance | $100m | -$5m | $95m |

| – Goods | $100m(1) | $100m | |

| – Services | -$5m(2) | -$5m | |

| Primary income balance | |||

| Secondary income balance | |||

| Capital account | |||

| Capital transfers | |||

| Acquisition/disposal of non-produced | |||

| non-financial assets | |||

| Financial account | $25m | -$120m | -$95m |

| Direct investment | |||

| Portfolio investment | -$20m(3) | -$20m | |

| Other investment | $5m(2) | -$100m(1) | -$75m |

| $20m(3) | |||

| Reserve assets | |||

| Net errors and omissions | |||

| Balance of payments | $125m | -$125m | $0m |

| * Example number indicated in brackets. | |||

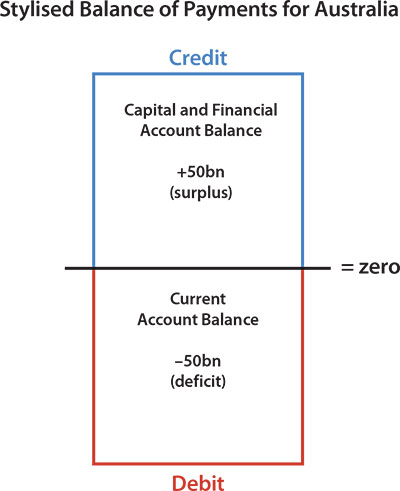

The Relationship Between the Accounts

The current account is always offset by the capital and financial account so that the sum of these accounts – the balance of payments – is zero. The logic underlying this, and represented in the double-entry accounting framework, is that the value of whatever is traded (recorded in the current account) is offset by a movement of some form of asset to pay for it (recorded in the capital and financial account). Consequently, when the balance of one account is in surplus (i.e. has a positive value, representing a credit), the balance of the other account must be in deficit (i.e. has a negative value, representing a debit).

We can summarise the relationship between the accounts with an example of Australian economic developments. Australia has tended to borrow from overseas, reflecting investment in the Australian economy. The capital flowing into Australia is recorded as a credit in the balance of payments and has been associated with a capital and financial account surplus. This surplus is matched by a current account deficit (recorded as a debit). Part of the reason for Australia's current account deficit is the interest Australia pays to the rest of the world on its international borrowing.