2014/15 Assessment of ASX Clearing and Settlement Facilities 6. Special Topic – Recovery Planning

Recovery plans are developed by an FMI within the framework of its rules and contractual arrangements to provide for a return to viability in the event of an extreme financial shock. The Bank's FSS require that CCPs and SSFs develop and maintain recovery plans in order to ensure that they could continue to provide critical clearing and settlement services following a threat to their continued viability. In the case of CCPs, recovery plans include arrangements to address shocks that go beyond those assumed in stress testing (see Section 5).

The Bank's 2013/14 Assessment recommended that ASX Clear, ASX Clear (Futures), ASX Settlement and Austraclear take steps to enhance their recovery plans. In the case of the ASX CCPs, ASX Clear and ASX Clear (Futures), the recommended steps included the implementation of arrangements to fully address any uncovered credit losses and replenish financial resources following a participant default, as well as arrangements to fully meet any liquidity shortfall.

The recommendation noted ongoing international work by CPMI and IOSCO to provide guidance to the industry on recovery planning. This guidance was released in October 2014.[54] In the same week, ASX launched its consultation on a package of tools to enhance its ability to effectively recover from a participant default that exhausted the CCPs' prefunded financial resources. On 21 April 2015, ASX released a set of draft rule changes that incorporated its response to feedback from consultation. The final rule changes were lodged with ASIC on 1 September and are due to take effect on 1 October 2015.[55]

This section summarises the key recovery planning requirements in the FSS, provides an overview of ASX's forthcoming recovery plans and presents the Bank's assessment of these arrangements. ASX has made significant progress in enhancing its recovery arrangements and is found to have observed all relevant requirements of the FSS, with the exception of requirements related to replenishment. In the case of replenishment, ASX is found to have broadly observed the relevant requirements. The Bank has made a recommendation outlining further steps required for ASX to achieve full observance.

6.1 Overview of FSS Requirements

The majority of the Bank's FSS requirements related to recovery planning came into effect on 31 March 2014.[56] The core requirements for recovery planning and addressing non-default losses apply to both CCPs and SSFs, but the full range of requirements apply only to CCPs, which unlike SSFs are exposed to financial risks on the default of a participant. Extracts from the relevant FSS sub-standards for CCPs are included in Table 14 (see Section 6.3).

- Recovery plans. CCPs and SSFs are required to identify scenarios that could threaten their ongoing provision of critical services and prepare appropriate plans for recovery or orderly wind-down to address such scenarios (CCP Standard 3.5 and SSF Standard 3.5).

- Loss allocation and replenishment. CCPs are required to establish arrangements to fully address any losses resulting from the default of one or more participants, as well as replenish any financial resources employed to meet such losses (CCP Standard 4.8).

- Addressing a liquidity shortfall. CCPs are required to establish arrangements that would allow them to settle their payment obligations on time following the default of one or more participants. These include arrangements to address liquidity shortfalls that could not be addressed using ‘qualifying’ liquid resources alone (CCP Standard 7.9).[57]

- Addressing non-default losses and recapitalisation. CCPs and SSFs are required to hold or have access to sufficient liquid net assets backed by capital to cover potential losses arising from sources other than a participant default (i.e. general business risks) and to fund implementation of their recovery plans. The CCP or SSF should also maintain a viable plan for raising additional funds in order to ensure that it retains the required level of general business risk capital, including after a shock that depleted its capital (CCP Standards 14.3 and 14.5, and SSF Standards 12.3 and 12.5).

The Bank has advised ASX that it will apply the CPMI-IOSCO guidance in interpreting its application of the above requirements. The guidance is not prescriptive as to which recovery tools an FMI should adopt. Rather, it outlines a menu of potential recovery tools with reference to a set of desired characteristics:

- comprehensiveness – the set of tools should comprehensively address how the FMI would continue to provide critical services in all relevant scenarios

- effectiveness – each tool should be reliable, timely and have a strong legal basis

- transparency, measurability, manageability and controllability – the tools should be transparent and allow participants to measure, manage and control their exposure to the tools

- creating appropriate incentives – the tools should create appropriate incentives for the FMI's owners, direct and indirect participants, and other stakeholders

- minimising negative impact – the tools should be designed to minimise negative impact on participants and the broader financial system.

The assessment of ASX's recovery proposals presented in this section uses these desired characteristics as a guide. To support this assessment, the Bank engaged in a continuing dialogue with ASX during the development of its recovery proposals and met with a number of participants and end users to better understand the potential implications of the measures.

6.2 ASX's Recovery Framework

As noted in the 2013/14 Assessment, in early 2014 ASX developed a basic recovery plan based on its clearing and settlement (CS) facilities' existing powers. While this plan identified a number of tools available to ASX to partly address uncovered credit losses and liquidity shortfalls, replenish financial resources and address a non-default-related loss, it acknowledged that these tools were not sufficient to comprehensively address the full range of threats to the ASX CS facilities' continued provision of critical services as required by the new FSS. ASX's enhancements to its recovery planning arrangements, supported by forthcoming changes to the ASX CCPs' operating rules, are designed to address these previous shortcomings and ensure that ASX's recovery plans meet the requirements summarised in Section 6.1.

In the process of introducing recovery-related changes to the CCPs' operating rules, both ASX and the Bank consulted with participants and other stakeholders. These discussions revealed a wide range of views, but there was recognition among participants that recovery measures along the lines proposed were necessary to improve the resilience of ASX's clearing and settlement (CS) facilities to a very extreme shock. Stakeholder comments were largely directed towards questions of design, such as the appropriate mix of recovery tools, thresholds for activating the use of tools, and the ability to control or estimate contingent exposures. Stakeholders were also concerned about any potential prudential capital implications of tools.

The remainder of this section provides more detail on the tools proposed by ASX and notes how these align with the ‘desirable characteristics’ set out in the CPMI-IOSCO guidance (see Table 15 for a summary mapping of ASX's tools against these characteristics). The focus of this discussion is on recovery arrangements for the ASX CCPs, with the only element relevant to the SSFs being the discussion about tools to address non-default losses. As in the CPMI-IOSCO guidance the tools in ASX's recovery framework encompass: tools to allocate losses and restore a matched book following a participant default; tools to address a liquidity shortfall; replenishment tools; and tools to address a non-default-related loss.

6.2.1 Tools to allocate losses and restore a matched book following a participant default

The suite of tools included in ASX's proposals to allocate losses and restore a matched book are summarised in Box C and discussed in further detail below.

Box C: Summary of the ASX CCPs' Proposed Tools to Allocate Losses and Restore a Matched Book

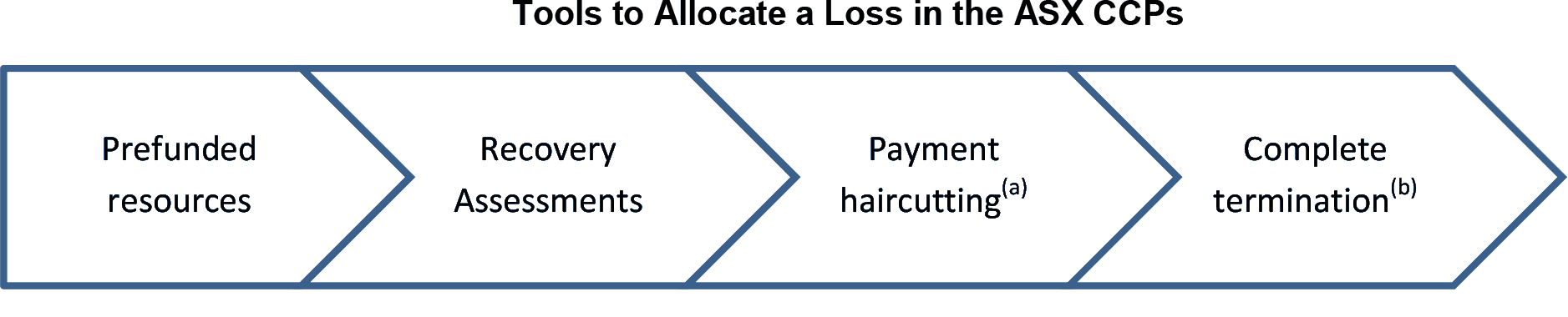

The ASX CCPs maintain prefunded financial resources (such as participant margin and a pooled default fund) calibrated to cover the default of any two participants and their affiliates in extreme but plausible market conditions (see Section 3.3). However, in very extreme cases it is possible that this prefunded financial cover could be insufficient to fully absorb default-related losses, leaving the CCP with an uncovered credit loss. ASX's proposed approach for allocating such an uncovered credit loss following a participant default differs between the two CCPs, but applies the same basic sequencing (Figure 1). The two CCPs also apply similar approaches to restoring a matched book, although there is some flexibility in the sequencing of both tools to allocate losses and to restore a matched book.

(b) Complete termination can be used to store a matched book as well as to allocate a loss; partial termination is an alternative tool for restoring a matched book that would typically be contemplated prior to complete termination

In the event that prefunded financial resources were exhausted, the following tools would be available to the ASX CCPs.

- Recovery Assessments. The power to call for additional cash contributions from participants to meet uncovered losses, in proportion to the risk associated with positions held by participants prior to the default. Capped at $300 million in ASX Clear and $600 million in ASX Clear (Futures) (or $200 million for a single default).

- Payment haircutting. A tool allowing the CCP to reduce (haircut) outgoing payments to participants in order to allocate losses suffered on the defaulting participant's portfolio. For example, a haircut may be applied to variation margin payments due to participants with net in-the-money positions in the event of mark-to-market loss on the defaulter's portfolio. This haircutting power is uncapped at ASX Clear (Futures), but is not available at ASX Clear due to the characteristics of the products that it clears.

- Partial termination. A power which could be used to close out a CCP's market risk on the defaulter's portfolio if normal close-out processes were not available or proved ineffective. The CCP would identify (on a pro rata basis) positions held by non-defaulting participants that were opposite to those that the CCP had inherited from the defaulter. These positions would then be terminated at their current market value, restoring the CCP to a matched book.

- Complete termination. A reserve power that could be used to restore a matched book and/or allocate losses if none of the above tools proved effective. Complete termination would involve tearing up all open contracts at the CCP and settling them at their current market value. Any residual losses of the CCP could be allocated by haircutting settlement payments to participants. Use of this tool would have a highly disruptive effect on the markets served by the CCP, so would be considered only as a last resort.

Loss allocation

As noted in ‘Box C: Summary of the ASX CCPs’ Proposed Tools to Allocate Losses and Restore a Matched Book', both CCPs would initially seek to allocate uncovered losses via Recovery Assessments. ASX Clear has a pre-existing assessment power in its rules. ASX Clear (Futures) did not previously have such a power.

- For ASX Clear (Futures), assessments would be capped at $200 million per participant default, up to a maximum of $600 million for multiple defaults within a defined ‘default period’.[5] This represents a maximum of 31 per cent of the ASX Clear (Futures) default fund in the case of a single default, or 92 per cent in the case of multiple defaults.

- For ASX Clear, assessments would be capped at $300 million for one or multiple defaults. ASX Clear's assessment power represents 120 per cent of its default fund.

The different levels of coverage achieved under the CCPs' respective Recovery Assessment powers reflect that ASX Clear (Futures) has additional loss allocation tools available if assessments were exhausted.

In the case of ASX Clear (Futures), if the CCP reasonably expects that losses may exceed default resources, including Recovery Assessments, the CCP could start haircutting gains-based payments to participants with net in-the-money positions (payment haircutting). While the largest payment obligations subject to a haircut would generally be variation margin payments, ASX has expanded the range of payments potentially subject to a haircut in response to feedback from stakeholders, including, for instance, net interest payments resulting from a rate reset. ASX would also have the discretion to retain a portion of default resources, including those raised via assessments, while carrying out payment haircutting, to meet any costs of settling an auction or other losses associated with closing out the defaulting participant's positions.

It is not proposed that ASX Clear would have the ability to haircut (variation margin) payments. This is because variation margin is applied differently to the products cleared by ASX Clear, and in general is collected on losses but not paid out on gains. Instead, ASX Clear has a more extensive assessment power that more than doubles its capacity to absorb losses above the defaulting participant's margin. If assessment funds were nevertheless exhausted in ASX Clear, it would allocate remaining losses by terminating all open contracts (see below) and applying a haircut to any settlement payments to participants.

Graph 12 illustrates how loss allocation tools relate to the overall default waterfalls of each CCP. In the event that the two largest participants defaulted, the first layer of loss absorbency would be the initial margin posted by those two participants, calibrated to cover losses to a 99.7 per cent confidence interval. The pooled default fund of each CCP would be used to absorb any losses that resulted from more extreme market conditions, calibrated to cover 99.98 per cent of the distribution of price moves.[6] In even more extreme conditions, assessments would provide coverage up to an estimated 99.998 per cent (once-in-200-year) confidence level in ASX Clear, or 99.992 per cent (once-in-50-year) confidence level in ASX Clear (Futures).

Characteristics of loss allocation tools

The loss allocation tools at the two CCPs are assessed to meet each of the desirable characteristics of recovery tools set out by CPMI and IOSCO.

-

Comprehensiveness. Both CCPs maintain loss allocation arrangements that can comprehensively allocate an uncovered loss arising from a participant default.

— ASX Clear relies primarily on assessments to allocate uncovered losses; ASX modelling indicates that these would be sufficient to allocate uncovered losses following the default of the two largest participants in a once-in-200-year market stress event. In circumstances involving even more extreme market moves or more than two participant defaults in very extreme market conditions, ASX Clear could still allocate remaining losses via its complete termination power.

— ASX Clear (Futures) can comprehensively allocate nearly all uncovered losses via a combination of assessments (covering the default of the two largest participants in a once-in-50-year market stress event) and payment haircutting. Complete termination can be used to allocate any remaining losses that are generated from sources other than payment flows and cannot be met by other resources (including assessments).

-

Effectiveness. The tools available to each CCP are designed to be reliable, timely and have a strong legal basis.

— Assessment obligations are payable on a next-day basis and are enforceable under the CCPs' rules. A failure to meet assessment obligations is an act of default and would enable the CCP to use the non-performing participant's initial margin to offset any assessment shortfall.

— Payment haircuts are applied to reduce settlement of payment obligations by an amount equal to the losses that need to be allocated. There is no risk of non-performance since the haircut operates as a reduction in amounts payable by the CCP rather than an obligation of the participants to pay in any funds.

— ASX has carried out analysis on the legal basis for its loss allocation tools. This analysis has not identified any material legal risk to enforceability of the assessment and payment haircutting powers or the application of protections under Part 5 of the PSNA to payment haircutting. ASX has recommended amendments to the PSNA to remove any uncertainty that protections under the PSNA would apply in the unlikely event that an assessment was called from a participant that itself later entered insolvency. This change is currently under consideration by Treasury.

-

Transparency and controllability. In the Bank's view, the tools available are transparent, allowing participants to measure, manage and control their exposures.

— Participants have a capped exposure to assessments.

— Potential exposure to payment haircutting can be controlled, since it is related to the size of participant's positions; ASX provides participants with sufficient information to allow them to calculate their potential exposures.

- Incentives. Both assessments and payment haircutting are linked to the positions held by participants, which assists in creating appropriate incentives for participants and their clients to manage the risk that they bring to the CCPs. Caps on assessments also reduce the risk that participants will exit central clearing, which they might have an incentive to do if they had a potentially uncapped exposure in the event of recovery.

- Minimising negative impact. The proposed sequencing of tools would be expected to limit the potential for negative impact on participants and the broader financial system. Assessments distribute losses widely among participants in proportion to their level of activity. While payment haircutting concentrates losses in fewer participants, it would be unlikely to trigger by itself further participant defaults except in the most extreme cases. Research undertaken by the Bank based on global derivatives exposures suggests that losses allocated via payment haircutting would still be widely dispersed, which should limit the potential for the transmission of stress.[60] The most severe impact, from complete termination, would be reserved for very extreme cases only.

Restoring a matched book

Both CCPs would have the power to force the settlement or termination of some or all open contracts in order to restore a matched book if the defaulter's positions could not be closed out in the market or by auction. While both CCPs already have partial termination powers in relation to their exchange-traded derivatives, ASX will extend these powers to OTC derivatives and cash market transactions. In addition, ASX is introducing a power to simultaneously terminate all open contracts as a last resort should other tools prove ineffective (complete termination).

ASX's partial termination powers align with a set of safeguards for the use of this tool as set out by the International Swaps and Derivatives Association (ISDA) in a January 2015 discussion paper.[61] In this paper, ISDA expressed cautious support for the use of partial termination as a final alternative to complete termination, which could have a highly disruptive effect. ISDA's support was conditional on three safeguards being met:

- the contracts terminated should be selected on a pro rata basis to diffuse its impact among multiple participants

- terminated contracts should be settled at market value

- partial termination should not be used to allocate losses.

These safeguards address industry concerns that participants with directional positions would be more exposed to the use of this tool, and seek to mitigate the risk that partial termination could lead to unpredictable effects on net exposures if some contracts were selected for termination while leaving offsetting contracts in place. ISDA's safeguards are also designed to avoid partial termination powers interfering with the accounting and capital treatment of net positions.

Characteristics of tools to restore a matched book

The tools to restore a matched book at the two CCPs are assessed to meet each of the desirable characteristics of recovery tools set out by CPMI and IOSCO.

- Comprehensiveness. The combination of partial and complete termination powers should ensure that both CCPs could restore their matched books in extreme circumstances.

- Effectiveness. Partial and complete termination powers could be applied in a timely and reliable manner, since ASX has the power to unilaterally force the settlement of open contracts to restore its matched book. ASX's legal analysis has not identified any material legal risk to enforceability of these powers or the application of protections under Part 5 of the PSNA.

- Transparency and controllability. Partial termination would be applied on a pro rata basis, allowing participants to manage and control their exposure to the tools via the size of their positions. An element of unpredictability would nevertheless remain since participants' net positions could be partially unwound. The impact of complete termination is fully transparent since all positions would be affected.

- Incentives. The threat of termination powers should provide incentives for participants to support default management processes. For example, uncertainty as to the impact of partial termination, or the threat of complete termination, could provide an incentive for participants to bid competitively in the auction of a defaulting participant's portfolio.

- Minimising negative impact. The availability of partial termination as an alternative to complete termination (where feasible) should limit the likelihood that the latter would be required to restore a matched book. This would allow the CCP's matched book to be restored in the least harmful way possible.

6.2.2 Tools to address a liquidity shortfall

ASX's arrangements to address a liquidity shortfall differ significantly between the two CCPs, reflecting the different liquidity risk profiles associated with the products that each CCP clears.

The primary liquidity obligations faced by ASX Clear (Futures) relate to the daily mark-to-market process. Accordingly, once pre-funded liquidity and liquidity sourced from Recovery Assessments were exhausted, payment haircutting would provide ASX Clear (Futures) with the means to comprehensively address any liquidity shortfall.

ASX Clear has an additional existing tool to address any liquidity shortfall associated with the settlement of securities transactions – OTAs. This tool is effectively a rules-based stock repurchase arrangement under which ASX Clear may source liquidity from participants that are due to deliver securities for settlement, using those securities as collateral for the liquidity that they provide. The transaction unwinds the next day.[62] As a last resort, complete termination could be used to address any remaining liquidity shortfall.

Liquidity risk on ASX Clear's derivatives trades is more limited than for ASX Clear (Futures) since it collects but does not pay out variation margin on most products. For remaining liquidity obligations, including variation margin payments on the few products for which gains are paid out, once pre-funded liquidity and an existing $150 million liquidity line were exhausted, ASX Clear would rely on funds received from Recovery Assessments ($300 million). If these resources still proved insufficient, any remaining liquidity shortfall would be addressed via complete termination.

Characteristics of tools to address a liquidity shortfall

The tools to address a liquidity shortfall at the two CCPs are assessed to meet each of the desirable characteristics of recovery tools set out by CPMI and IOSCO.

- Comprehensiveness. The combination of assessments and payment haircutting (for ASX Clear (Futures)) or OTAs (for ASX Clear) provide a comprehensive means of addressing a liquidity shortfall. Any residual shortfall in ASX Clear related to derivatives transactions could be addressed via complete termination.

- Effectiveness. OTAs could be applied in a timely and reliable manner, since this tool would be applied directly to ASX's payment obligations to selling participants, which would not be required to pay in any funds. ASX's legal analysis has not identified any material legal risk to enforceability of OTAs or the application of protections under Part 5 of the PSNA.

- Transparency and controllability. Participants are able to manage and control their exposure to OTAs via the size of their cash market positions. The Bank is continuing to discuss with ASX how better to disclose the potential impact of OTAs to participants, since this in part depends on the application of ASX's ‘back-out’ algorithm to select trades to be offset (see Section 3.5.1).[63]

- Incentives. OTAs should provide incentives for participants to manage the level of risk they bring to the CCP, since this risk is linked to the size of participant positions (albeit with adjustments via the back-out algorithm to minimise the flow-on effects to batch settlement).

- Minimising negative impact. Obligations under OTAs are calibrated (via the back-out algorithm) to minimise the liquidity impact on participants in ASX Settlement's daily batch process.

Other tools are the same as those used to allocate an uncovered loss – the characteristics of these tools are described in the context of loss allocation tools.

6.2.3 Replenishment

ASX has developed a staged process for replenishment of the CCP default funds in the event that these were exhausted or partially drawn on following a participant default. For each CCP, irrespective of whether the default fund was fully or only partially depleted, participants would be given a 17 business-day period from completion of the default management process to determine whether they wished to contribute to replenishment, or instead close out their existing positions and resign from the CCP at the conclusion of the default period. Participants that had not exited their existing positions and provided notice of resignation at the conclusion of the 17 business days would be required to contribute to replenishment of the default fund in proportion to their activity prior to the default. During this period, ASX would rely on initial margin and any remaining default fund resources to cover the CCP's exposures to a subsequent participant default.[64] ASX would also have the discretion to call AIM from participants based on their stressed exposures, although this would place a greater liquidity burden on participants than a replenishment undertaken on a mutualised basis (‘ Box D: Liquidity Impact of Replenishment’). This could be procyclical in the context of the stressed environment in which these events might eventuate.

Box D: Liquidity Impact of Replenishment

The design of ASX's replenishment arrangements has implications for the timing and magnitude of liquidity obligations placed on its participants. This box discusses these implications and illustrates them using a stylised hypothetical example.

The purpose of replenishment arrangements is to ensure that a CCP can return to its full level of financial cover, which in the case of the ASX CCPs requires sufficient financial resources to cover the default of the two participants that would give rise to the greatest joint loss in extreme but plausible market conditions (Cover 2). While a prompt return to Cover 2 should be a key objective of a CCP's replenishment approach, replenishment arrangements should take into account the relative risks to participants from, and liquidity impact of, reliance on either pooled or non-pooled resources, or a combination of the two.

- Non-pooled resources (e.g. initial margin and AIM) avoid exposing participants to potential loss from a fellow participant default. However, since non-pooled resources can be used only to meet losses arising from the default of the participant that provided them, a greater quantum of resources is required to provide the same level of coverage than would be the case for pooled resources.

- Pooled resources (e.g. default fund contributions) would be exposed to loss if a defaulting participant's non-pooled resources proved insufficient to meet losses on its positions. However, a lower level of funds would be required from participants to return the CCP to Cover 2 than would be the case for non-pooled resources.

For example, if a CCP had 10 identical participants with stressed exposures of $100 million each, each participant would be required to provide $100 million in AIM to return the CCP to Cover 2 (Table D1). In this case there is no distinction between the CCP covering stressed exposures to one or all participants, since AIM provided by one participant cannot be used to meet stressed losses of another participant. Alternatively, the CCP could seek a return to Cover 2 via pooled resources. At most this would require the CCP to rebuild its default fund to $200 million, assuming that at least two participants held positions subject to common stresses.[1] In the case of a CCP, such as one of the ASX CCPs, that committed to contributing half of this amount, participants would face a replenishment obligation of $10 million each.

| Non-pooled resources (AIM) | Pooled resources(b) | |

|---|---|---|

| Aggregate contribution required | $1,000 m | $200 m |

| Contribution per participant | $100 m | $10 m |

| CCP contribution | – | $100 m |

| (a) Assumes 10 participants with stressed losses of $100m each, with at

least two participants holding positions in the same direction (b) Assumes the CCP contributes 50 per cent of the replenished default fund |

||

This stylised example illustrates the heightened liquidity impact on participants – and, therefore, the system more generally – from a reliance on non-pooled resources (such as AIM) to return a CCP to Cover 2. The liquidity impact on participants from reliance on non-pooled resources will be greatest relative to the use of pooled resources where:

- there is a larger number of participants, each of which will need to post AIM on its individual stressed exposures

- the distribution of stressed losses among participants is relatively even, since pooled resources are based only on the two participants with the largest joint exposure

- the CCP contributes a significant portion of pooled resources.

If the funds were fully depleted, ASX would match, dollar-for-dollar, contributions made by participants to re-establish default funds of up to $400 million in ASX Clear (Futures) and $150 million in ASX Clear. ASX's plans to fund these contributions include the use of existing cash reserves and/or raising additional capital through equity issuance. The Bank has commenced discussions with ASX to better understand these plans, which might need to be implemented in challenging circumstances.

The re-established default funds would initially be smaller than the current default funds in each CCP, on the presumption that the exposures of surviving participants would be smaller. If stress testing demonstrated that the re-established default funds did not adequately cover post-recovery exposures, ASX would have the capacity to call additional participant and ASX contributions to restore the default funds to pre-recovery levels as part of a recalibration at the end of the quarter. This ‘scaling-up’ process would apply the same 50/50 split of ASX and participant contributions as would apply to the initial post-recovery default fund. ASX is also removing the requirement for a participant ballot to approve an increase in participant default fund contributions if required to scale up the level of financial cover. In the meantime, if post-recovery exposures were not adequately covered, ASX would rely on AIM calls on participants.

In the event that the default fund was partially drawn on rather than fully exhausted, replenishment would occur from a higher base. As in the case of a fully depleted fund, ASX would initially contribute up to $75 million in ASX Clear and $200 million in ASX Clear (Futures), with participants again contributing up to the same amount. If this was insufficient to provide the required level of cover, ASX would again rely on the use of additional margin until the default fund could be scaled up. The post-replenishment composition of the default fund would depend on the amount to be replenished; the larger the initial drawdown, the closer would be the post-replenishment composition to a 50/50 split of ASX and participant contributions. In the case of a drawdown of less than $75 million in ASX Clear, ASX would meet the entire replenishment requirement, preserving the current default fund composition of 100 per cent of ASX funds.

Characteristics of replenishment tools

The replenishment tools at the two CCPs are assessed to meet only some of the desirable characteristics of recovery tools set out by CPMI and IOSCO.

- Comprehensiveness. The provisions for both participant and ASX contributions to replenishment provide a path for both CCPs to return to full cover over time.

- Effectiveness. The approach to replenishment may not be timely, since there would be a delay of at least 22 business days before the CCPs returned to full mutualised cover (potentially longer if a subsequent ‘scaling up’ of the default fund was required). The Bank is continuing to discuss with ASX its plans to fund its own contribution to replenishment to ensure that this would be reliable in stressed conditions. ASX has carried out analysis on the legal basis for its replenishment plans. This analysis has not identified any material legal risk to the enforceability of replenishment powers. ASX has recommended amendments to the PSNA to remove any uncertainty that protections under the PSNA would apply in the unlikely event that a replenishment contribution was called from a participant that itself later entered insolvency. This change is currently under consideration by Treasury.

- Transparency and controllability. Participants are aware of the full extent of their replenishment obligations in advance, and could avoid replenishment by resigning their participation in the CCP.

- Incentives. The current design of replenishment obligations could create inappropriate incentives for participants to resign, since these obligations are initially linked to pre-default positions and could be controlled only by exiting the CCP entirely. Nevertheless, the strength of this incentive is limited by the cap on participants' replenishment contributions.

- Minimising negative impact. The approach to replenishment would allow participants sufficient time to obtain approvals and funding to meet their obligations. However, the use of additional margin to manage risk in the interim (22 business-day period) could potentially transmit procyclical liquidity stress by requiring participants to post more collateral than would be the case under mutualised cover.

6.2.4 Non-default losses

Non-default losses could arise from losses on treasury investments or a range of general business risks.

- In the case of investment losses, ASX would apportion any losses in excess of $75 million (an amount equal to the CCPs' general business risk capital) between participants in proportion to the amount of cash collateral each has provided to the CCP (both margin and default fund contributions).

- Other non-default, general business losses to the CCPs would be absorbed by ASX. Unlike investment losses, general business losses from causes such as a decline in revenues or an increase in operating expenses are likely to be relatively slow-moving in nature. In the case of the SSFs, which are only exposed to non-default, non-investment losses, remaining losses would likewise be absorbed by ASX, including through application of general business risk capital held for the SSFs by ASX Limited. ASX supplements its business risk capital through the use of insurance to cover its exposure to a broad range of risks (including coverage of professional indemnity and fraud risks). ASX Limited has also committed to maintaining adequate levels of business risk capital for the CCPs and SSFs, recapitalising these funds as required.

Characteristics of tools to address a non-default loss

The tools to address a non-default loss at the two CCPs are assessed to meet each of the desirable characteristics of recovery tools set out by CPMI and IOSCO.

- Comprehensiveness. Investment losses in excess of business risk capital could be comprehensively addressed via allocation to participants. Other non-investment general business losses would be met via insurance or recapitalisation of general business risk capital used to absorb such losses.

- Effectiveness. The allocation of investment losses should be timely and reliable, since any allocation could be offset against participant collateral held at ASX. ASX's legal analysis has not identified any material legal risk to enforceability of investment loss allocation or the application of protections under Part 5 of the PSNA. Non-investment general business losses would typically be expected to be slower to crystallise, allowing time for ASX to process an insurance claim or raise additional capital.

- Transparency and controllability. Investment loss allocations would be proportional to the value of cash collateral posted by each participant, allowing participants to manage, measure and control their exposures to this tool. The Bank will discuss with ASX the disclosure of information on its investment risk profile to participants in the context of planned changes to ASX's treasury investment policy (see Section 3.5.4), in part to assist them in understanding their contingent exposure to investment losses. Participants would have no exposure to non-investment general business losses.

- Incentives. Investment loss allocations to participants would be proportional to the size of participants' positions with each CCP, strengthening incentives for participants to manage the level of risk they bring to the CCP. The residual exposure of participants to investment losses should provide them with incentives to monitor ASX's management of investment risks.

- Minimising negative impact. Allocating excess investment losses to participants on a pro rata basis spreads the impact of this tool as widely as possible.

6.2.5 Safeguards

ASX has incorporated a number of safeguards to govern its exercise of recovery measures, in recognition of the open-ended nature of some of the recovery tools described above, and the discretion held by ASX in exercising its recovery powers. While this flexibility is necessary for ASX to respond effectively to unpredictable circumstances in recovery, this elevates the importance of appropriate mechanisms for transparency and accountability in ASX's decision-making process. ASX therefore proposes to introduce requirements to consult with the Bank regarding any use of recovery tools, and with participant risk committees in each CCP in a broad range of circumstances. For instance, consultation with participant risk committees would be required where payment haircutting extended beyond seven business days or exceeded a certain value threshold, or when exercising partial or complete termination powers.

6.2.6 Updated recovery plan

Prior to its consultation on new recovery tools, ASX had documented a basic recovery plan based on its existing powers. It is in the process of updating this plan in line with the expanded set of recovery tools, alongside a broader refresh of its default management plan. ASX will also be giving consideration to how its recovery plan is maintained and tested on an ongoing basis.

6.3 Conclusions and Recommendations

ASX has made significant enhancements to its framework for recovery over the course of the Assessment period. The Bank's assessment is that ASX has observed all of the relevant minimum requirements in the FSS, with the exception of certain requirements related to replenishment. In the case of replenishment, ASX is found to have broadly observed the relevant requirements, with a recommendation for further action by ASX to achieve full observance. Other recommendations identify steps for continued monitoring and review, or reflect areas where ASX could enhance its observance of the relevant standards in the spirit of continuous improvement. ASX has already commenced work in many of the areas covered by the recommendations.

The Bank's ratings and recommendations are based largely on its analysis of ASX's recovery tools according to the desired characteristics of recovery tools set out in the CPMI-IOSCO guidance. This analysis, set out in Section 6.2, is summarised in Table 15. The key conclusions drawn by the Bank in performing its assessment are set out below.

-

Loss allocation. ASX's planned loss allocation arrangements are considered to strike an appropriate balance between the use of assessments, which are widely distributed but subject to performance risk, and other tools (payment haircuts or complete termination).

– ASX has provided modelling that indicates that assessments would be sufficient to cover two defaults during a once-in-50-year event for ASX Clear (Futures) or a once-in-200-year event for ASX Clear. In the latter case, this means that reliance on complete termination to allocate losses would be highly unlikely. Both CCPs have at least one uncapped loss allocation tool and therefore the full package of loss allocation measures is comprehensive.

– The application of uncapped payment haircutting in ASX Clear (Futures) when assessments have been exhausted minimises both performance risk and the direct liquidity impact on participants, since it does not rely on the paying in of additional funds. Although payment haircutting would result in a more uneven distribution of losses than assessments,[65] Bank research suggests that the potential for the transmission of stress would remain limited. ASX has undertaken to provide the Bank with further quantitative analysis to assist in validating the potential impact of payment haircutting based on historically observed participant positions in ASX Clear (Futures).

- Restoring a matched book. The Bank's view is that ASX's arrangements provide an appropriate suite of tools to restore a matched book. The amendments to partial termination powers align with industry expectations voiced by ISDA and provide a potentially less disruptive means of restoring a matched book than complete termination. It is appropriate to retain complete termination as a reserve power. However, once the proposed special resolution regime for FMIs comes into effect, the Bank would have the capacity to intervene if other recovery tools were proving ineffective and complete termination was under consideration.

- Addressing liquidity shortfalls. The Bank's assessment is that arrangements for addressing a liquidity shortfall in ASX Clear (Futures) are appropriate. The Bank also considers that ASX Clear's arrangements for addressing a liquidity shortfall on cash equity positions are appropriate, and has obtained analysis from ASX to support its proposed use of complete termination as a last resort to address a residual liquidity shortfall on derivatives positions in ASX Clear. ASX's analysis demonstrates that the prospect of relying on complete termination is extremely remote.

-

Replenishment. ASX's arrangements for replenishment would delay the return to a default fund that provided cover consistent with FSS requirements for at least 22 business days. Feedback from consultation suggested that more rapid (full) replenishment would not be possible for many participants. It is the Bank's view, however, that ASX should be able to return to regulatory minimum levels of default cover on a more rapid basis, consistent with the CPMI-IOSCO guidance that CCPs should have the capacity to return to full cover on a next-day basis if practicable.[66] This need not take the form of a committed fixed contribution, as would be the case for full replenishment, but could for instance be at least partly in the form of additional margin calls. While ASX has the capacity to call such margin, sole reliance on margin to cover stressed exposures could be highly procyclical. At the same time, in stressed market circumstances, participants might prefer to bear the liquidity cost of additional margin rather than face the risk of a loss on any additional contribution they might make to mutualised resources.

The Bank has signalled to ASX the need for further work on replenishment, in order to facilitate a more timely return to full cover while minimising the potential for procyclicality. There may be a range of approaches that could be used to meet these objectives in an achievable way. As part of this work, ASX will also need to satisfy the Bank that it has credible arrangements in place to fund its replenishment obligations in stressed circumstances. If not, an alternative ex ante default fund composition that relies less on ASX capital might need to be considered.

- Non-default losses. The arrangements for allocating investment losses are considered to be appropriate, provided that ASX implements plans to reduce its exposures to non-government investment counterparties and issuers (see Section 3.5.4). The reliance on insurance and recapitalisation of the CS facilities' general business risk capital to address residual uncovered non-investment losses is also considered to be appropriate on the basis that (i) such residual losses would be expected to be extremely remote, and (ii) they would accrue gradually over time rather than arising on a short unanticipated timeframe.

Table 14 summarises the Bank's assessment of the ASX CCPs against the specific sub-standards of the FSS that address matters related to recovery planning, applying the rating system described in Section 2.2. Table 14 includes the Bank's recommendations and identifies areas in which the Bank will continue to monitor developments during the 2015/16 Assessment period.

| Standard | Rating | Recommendation |

|---|---|---|

| 3.5. Preparation of recovery plans A central counterparty should identify scenarios that may potentially prevent it from being able to provide its critical operations and services as a going concern and assess the effectiveness of a full range of options for recovery or orderly wind-down. A central counterparty should prepare appropriate plans for its recovery or orderly wind-down based on the results of that assessment. Where applicable, a central counterparty should also provide relevant authorities with the information needed for purposes of resolution planning. |

Observed | ASX is encouraged to complete planned updates to the documentation of its

recovery plans to take into account its expanded suite of recovery tools. ASX is encouraged to integrate testing and review of its recovery plan into its broader framework for testing and review of risk management and default management policies and processes. The Bank will monitor the outcomes from this testing and review process. |

| 4.8. Loss allocation and replenishment A central counterparty should establish explicit rules and procedures that address fully any credit losses it may face as a result of any individual or combined default among its participants with respect to any of their obligations to the central counterparty. These rules and procedures should address how potentially uncovered credit losses would be allocated, including the repayment of any funds a central counterparty may borrow from liquidity providers. These rules and procedures should also indicate the central counterparty's process to replenish any financial resources that the central counterparty may employ during a stress event, so that the central counterparty can continue to operate in a safe and sound manner. |

Broadly observed | In order to fully observe CCP Standard 4.8, ASX should complement its comprehensive

loss allocation arrangements by further refining its replenishment arrangements

to ensure that it is able to return to the full level of cover required

under CCP Standard 4.4 on a more timely basis, while minimising the potential

for procyclicality. ASX is also encouraged to test and review its capacity

to replenish its own contribution to the CCP default funds. ASX is encouraged periodically to review its loss allocation arrangements, to ensure that these continue to strike an appropriate balance in terms of comprehensiveness, effectiveness, transparency and controllability, creating appropriate incentives and minimising negative impact. ASX is encouraged to carry out plans to develop additional disclosures to assist participants in understanding their contingent exposure to the use of loss allocation tools. |

| 7.9. Addressing a liquidity shortfall A central counterparty should establish explicit rules and procedures that enable the central counterparty to effect same-day and, where appropriate, intraday and multiday settlement of payment obligations on time following any individual or combined default among its participants. These rules and procedures should address unforeseen and potentially uncovered liquidity shortfalls and should aim to avoid unwinding, revoking or delaying the same-day settlement of payment obligations. These rules and procedures should also indicate the central counterparty's process to replenish any liquidity resources it may employ during a stress event, so that it can continue to operate in a safe and sound manner. |

Observed | ASX is encouraged periodically to review its arrangements to address a liquidity

shortfall, to ensure that these continue to strike an appropriate balance

in terms of comprehensiveness, effectiveness, transparency and controllability,

creating appropriate incentives and minimising negative impact. ASX is encouraged to carry out plans to develop additional disclosures to assist participants in understanding their contingent exposure to the use of tools to address a liquidity shortfall. |

| 14.3. Addressing non-default losses A central counterparty should maintain a viable recovery or orderly wind-down plan and should hold or have legally certain access to, sufficient liquid net assets funded by equity to implement this plan. At a minimum, a central counterparty should hold, or have legally certain access to, liquid net assets funded by equity equal to at least six months of current operating expenses. These assets are in addition to resources held to cover participant defaults or other risks covered under CCP Standard 4 on credit risk and CCP Standard 7 on liquidity risk. However, equity held under international risk-based capital standards can be included where relevant and appropriate to avoid duplicate capital requirements. |

Observed | ASX is encouraged periodically to review its arrangements to allocate investment-related losses, to ensure that these continue to strike an appropriate balance in terms of comprehensiveness, effectiveness, transparency and controllability, creating appropriate incentives and minimising negative impact. |

| 14.5. Recapitalisation A central counterparty should maintain a viable plan for raising additional equity should its equity fall close to or below the amount needed. This plan should be approved by the board of directors and updated regularly. |

Observed | ASX is encouraged to test and review its capacity to raise additional equity to replenish general business risk capital. |

| Comprehensiveness | Effectiveness | Transparency and controllability | Creating appropriate incentives | Minimising negative impact | |

|---|---|---|---|---|---|

| Loss allocation tools | |||||

| ASX Clear | Met via a combination of assessments and haircuts on complete termination. Assessments calibrated to cover two defaults in a 1-in-200 year event. | Met via next-day payment of assessments, which are calibrated based on participant activity. Failure to meet assessment obligations is an act of default. Legal basis founded in Operating Rules, approved as a netting market under the PSNA. | Met. Exposure to assessments and complete termination is fully transparent to participants. | Met. Avoiding ex-ante commitment to uncapped emergency assessments should reduce the risk that participants exit central clearing. | Met. Assessments distribute losses widely based on participant activity; complete termination triggered only in very extreme circumstances. |

| ASX Clear (Futures) | Met via a combination of assessments and uncapped payments haircutting. Haircuts on complete termination available to address any residual losses. | Met via next-day payment of assessments, which are calibrated based on participant positions. Payment haircuts have no performance risk. Legal basis founded in Operating Rules, approved as a netting market under the PSNA. | Met. Exposure to assessments and complete termination is fully transparent to participants. ASX intends to provide additional reporting on potential exposure to payment haircutting, which is controllable since it is based on participants' outstanding positions. | Met. Linking payment haircutting (which affects direct and indirect participants) and emergency assessments to the size of positions creates incentives for both clearing members and clients to manage exposures. | Met. Assessments distribute losses widely based on participant activity. Payment haircutting could transmit stress, but would be unlikely to trigger further defaults except in the most extreme cases. Complete termination would be triggered only if other tools prove ineffective. |

| Tools to re-establish a matched book | |||||

| ASX Clear, ASX Clear (Futures) | Met via a combination of partial and complete termination powers. | Met. ASX has the power to unilaterally force the settlement of open contracts to restore its matched book. Legal basis founded in Operating Rules, approved as a netting market under the PSNA. | Met. ASX proposes to apply partial termination on a pro rata basis, although an element of unpredictability will remain. Complete termination is fully transparent to participants. | Met. The threat of termination powers should provide incentives for participants to support default management processes. In respect of an over-the counter contract auction, uncertainty as to the impact of partial termination, or the threat of complete termination, may provide an incentive to bid competitively. | Met. The ability to partially terminate where feasible minimises the likelihood that complete termination will be required. |

| Tools to address a liquidity shortfall | |||||

| ASX Clear | Met via a combination of assessments and OTAs for securities, if prefunded resources and liquidity lines proved insufficient. Residual shortfalls would be met via complete termination. | Met. OTAs have no performance risk. Legal basis founded in Operating Rules, approved as a netting market under the PSNA. | Met. Exposure to OTAs is controllable since this is a position-based tool; however, the Bank is continuing to discuss with ASX how better to disclose the potential impact of OTAs to participants. | Met. OTAs are linked to the size of participant positions, albeit not with a one-to-one relationship. | Met. Obligations under OTAs would be calibrated to minimise the liquidity impact on participants in ASX Settlement's daily batch settlement process. |

| ASX Clear (Futures) | Met via a combination of assessments and payment haircutting, if prefunded resources proved insufficient. | Met. See discussion of assessments and payment haircutting under ‘Loss allocation tools’ | |||

| Replenishment | |||||

| ASX Clear, ASX Clear (Futures) | Met. The proposals provide a path to return to full cover over time. | Further work required. There is delay of at least 22 business days in returning to full mutualised cover. Plans to raise additional ASX capital for timely replenishment may not be reliable in stressed conditions. | Met. Replenishment obligations are fully transparent to participants and may be avoided by resignation. | Further work required. Linking replenishment obligations to pre-default positions may create incentives to resign. | Further work required. The longer period for replenishment allows participants sufficient time to meet obligations; however, use of additional margin to manage risk in the interim could transmit liquidity stress. |

| Tools to address non-default losses | |||||

| ASX Clear, ASX Clear (Futures) | Met. The proposals fully address investment losses in excess of business risk capital; other non-investment general business losses would be met via insurance or recapitalisation. | Met. Investment loss allocations can be offset against collateral held at ASX. Legal basis founded in Operating Rules, approved as a netting market under the PSNA. | Met. Investment loss allocations proportional to cash posted as collateral. | Met. Investment loss allocations proportional to positions and provide incentives to monitor ASX's management of investment risks. | Met. Pro rata allocations spread the impact as widely as possible. |

Footnote Box D

In practice, it is not necessarily the case that the two participants giving rise to the highest individual stressed losses will be the participants used to size financial resources on a Cover 2 basis. The two participants with the largest absolute stressed exposure may hold opposing positions that would result in a lower net exposure in the event of a joint default. [1]

Footnotes

See CPMI-IOSCO (2014), Recovery of Financial Market Infrastructures, Bank for International Settlements, Basel, available at <http://www.bis.org/cpmi/publ/d121.htm>. The strengths and weaknesses of the tools described in the CPMI-IOSCO guidance are discussed in Gibson M (2013), ‘Recovery and Resolution of Central Counterparties’, RBA Bulletin, December, pp 39–48. [54]

Implementation is subject to the relevant Minister's power, under Section 822E of the Corporations Act, to disallow rule changes within 28 days of lodgement with ASIC. [55]

While the Bank's new FSS came into effect on 29 March 2013, the requirements related to recovery (other than CCP Standard 14.5) were among a small number of standards that were subject to 12 months of transitional relief. This relief reflected that observance of these requirements was partly dependent on the development of international guidance on recovery planning then underway. [56]

Qualifying liquid resources for the purpose of the FSS are defined under CCP Standard 7.4. [57]

The default period concludes 22 business days after the conclusion of the final default management process initiated during the period. Subsequent defaults within this period would therefore extend the default period by a further 22 business days from the point at which the subsequent default management process was successfully concluded. [58]

Section 5 explains in more detail how the default funds are calibrated using stress testing. The estimated confidence intervals for the default fund and assessments are based on historical price data, assuming a student t distribution where necessary to extrapolate prices beyond the sample used. [59]

See Heath, Kelly and Manning (2015), ‘Central Counterparty Loss Allocation and the Transmission of Financial Stress’, RBA Research Discussion Paper No 2015-02, available at <http://www.rba.gov.au/publications/rdp/2015/2015-02.html>. [60]

ISDA's discussion paper is available at <http://www2.isda.org/attachment/NzE5OQ==/CCP%20Default%20 Management%20recovery%20and%20continuity%2026-01-2015.pdf>. [61]

For a full description of OTAs, see Appendix A1.1, CCP Standard 7.3. [62]

The back-out algorithm selects trades to be removed from the CHESS batch where a participant fails to deliver securities, or trades to be offset by OTA trades where a participant fails to meet its payment obligation. The algorithm is designed to minimise the overall impact to the batch of removing or adjusting trades (see Appendix A2.1, SSF Standard 10.2). [63]

Any uncovered losses incurred in such circumstances would trigger the further use of loss allocation tools; for example, ASX Clear (Futures) could use payment haircutting to allocate remaining losses. [64]

Payment haircutting would, however, more closely reflect the likely distribution of losses under insolvency (see Gibson M (2013), ‘Recovery and Resolution of Central Counterparties’, RBA Bulletin, December, pp 39–48 for discussion of the distribution of losses under each of these scenarios). [65]

The guidance clarifies that practicability includes consideration of the potential procyclical impact of replenishment measures involving a call for additional financial resources from participants. [66]