Reserve Bank of Australia Annual Report – 1987 The Policy Framework

The economic setting

The process of correcting Australia's current account imbalance necessarily led to a significant slowing in economic growth in 1986/87. As the year progressed there were signs that necessary adjustments were taking place. But it was also clear that the task ahead is still substantial.

Slow growth in incomes, a reduced fiscal impetus, high interest rates and widespread uncertainty about economic prospects, including inflation, kept domestic demand subdued. Though the economy slowed, it did not move into general recession. Employment continued to grow sufficiently to keep the unemployment rate generally steady. The rate of price increases rose to almost 10 per cent before moderating somewhat later in the year. This contrasted with the average rate of inflation in the seven major OECD countries of around 2 per cent.

The external sector accounted for all the net growth in domestic product in 1986/87. Despite difficulties in some traditional markets and a slowing in world growth over the course of the year, Australia's export shipments were strong. Import volumes fell. This reflected restrained domestic demand and improved competitiveness resulting from the earlier fall in the value of the Australian dollar.

A further decline in the terms of trade partly offset the beneficial effects on the current account of the stronger volume performance. On the export side, wheat, iron ore and coal were the commodities whose prices were most affected. Even so, the net outcome for the current account in 1986/87 was a little better than expected.

There was again little growth in business investment in 1986/87, but investment in financial assets by Australians was strong, both at home and abroad. Despite the overall weakness in real investment in Australia, there were signs that resources were moving into growth sectors, particularly those boosted by exchange rate depreciation. These included tourism and some areas of manufacturing for export markets and import replacement.

The stockmarket boomed in terms both of volume and prices. Mergers and acquisitions were an important element. Foreign interest was strong as overseas investors sought to diversify their portfolios in the wake of a weakening U.S. dollar. Changes to the Government's foreign investment policy announced during the year encouraged investment by foreign government agencies as well as foreign private investors. Changes in Australian taxation policy have increased the prospective after-tax rate of return on investment in shares held by individuals resident in Australia. The introduction of a tax on capital gains may have led to some reluctance to sell on the part of long-term holders. Nevertheless, stockmarket turnover was at record levels.

Australian investment abroad also was at a high level in the year. This included some further portfolio adjustment following the suspension of exchange controls in 1983. Much of the investment was by institutional investors such as life offices and pension funds. Direct investment abroad by corporations seeking international expansion also was strong.

As 1986/87 progressed, moderate growth in the monetary aggregates and some signs of slowing in credit growth suggested that high interest rates were having an effect. Growth in M3 slowed, but was still more rapid than that of broad money; this was due in large part to the conversion of non-bank financial intermediaries to banks. In addition, the nature of a good deal of intermediation business has changed, making the traditional monetary aggregates based primarily on Australian dollar deposits increasingly difficult to interpret as indicators of financial conditions. Over the past year, “off-balance-sheet” activity has grown faster than balance-sheet-based financing. The commercial bill, bearing the acceptance or endorsement of a bank, which was revived some 25 years ago, continues as a major financial instrument. Offshore borrowing to finance lending in Australia was again an important source of funds for banks and other financial intermediaries. It was not found practicable during the year to amend the requirement on trading banks to hold a percentage of their deposit funds in Statutory Reserves with the Reserve Bank. This requirement (currently 7 per cent of deposits) increases the cost of raising conventional bank deposits and is an added incentive to the raising of funds in other forms or through other channels. This bears particularly on newer banks seeking to develop an Australian dollar deposit base.

1 INFLATION: AUSTRALIA AND MAJOR OECD COUNTRIES

These developments took place against a background of slowing world growth, persistent trade imbalances between the major industrial nations and growing protectionist sentiment. Currency markets were characterised by volatile short-term capital flows and considerable exchange rate instability as major industrial countries, particularly the United States, Japan and West Germany, struggled to find solutions to their current account imbalances. United States' external debt expanded rapidly as the U.S. absorbed savings from other industrial countries, particularly Japan and West Germany. The difficulties of some indebted developing countries added further uncertainty.

Progress on international policy co-ordination was slow. Despite statements of intent at several meetings held throughout the year, both domestic and external imbalances remained large in some key industrial countries. Intervention by their central banks sought to stabilise foreign exchange markets, but much volatility remained.

Australia's net external debt continued to rise in 1986/87, though in contrast to recent years its growth was slowed by the strengthening of the Australian dollar against the U.S. dollar. There was a welcome improvement in the trade account of the balance of payments. The current account position was also helped by the performance of the services sector, including tourism. On the other hand, debt servicing obligations have made sharply increased calls on export earnings over recent years; interest payments on Australia's net external debt accounted for over 18 per cent of export receipts in 1986/87, compared with less than 9 per cent five years ago.

Following financial deregulation, Australian investors have diversified the currency spread of their portfolios and overseas investors hold substantial Australian financial assets. Australian interest rates and exchange rates consequently are increasingly influenced by developments abroad.

The policy setting

At the beginning of 1986/87, it was clear that the Australian economy faced a need for major changes; there was a general expectation that firm, not to say harsh, measures would be required.

Policy actions announced with the 1986/87 Commonwealth Budget, as well as tightening the overall stance of policy, aimed to shift part of the burden of adjustment from monetary policy to fiscal and wages policies. A substantial cut in the Budget deficit was announced and further restraint of growth in labour costs was an important objective. But the public mood, initially, was sceptical. In the event, the fiscal measures and the implied reduction in the net public sector borrowing requirement were not regarded as sufficient to provide for immediate easing of monetary policy.

In March 1987, a two-tiered wage-setting system replaced the system of wage indexation introduced in 1983 under the Prices and Incomes Accord. This change held out the prospect of more flexible, but less certain, wage outcomes.

By the end of 1986/87, further initiatives had been announced by the Government to improve the policy mix. The Government's Economic Statement in May and the subsequent Premiers' Conference and Loan Council negotiations raised the prospect of a substantial fall in public sector demand for funds in 1987/88. The outcome for the Commonwealth deficit in 1986/87 was substantially below that expected at Budget time, reinforcing the prospect of reduced public sector demands for funds.

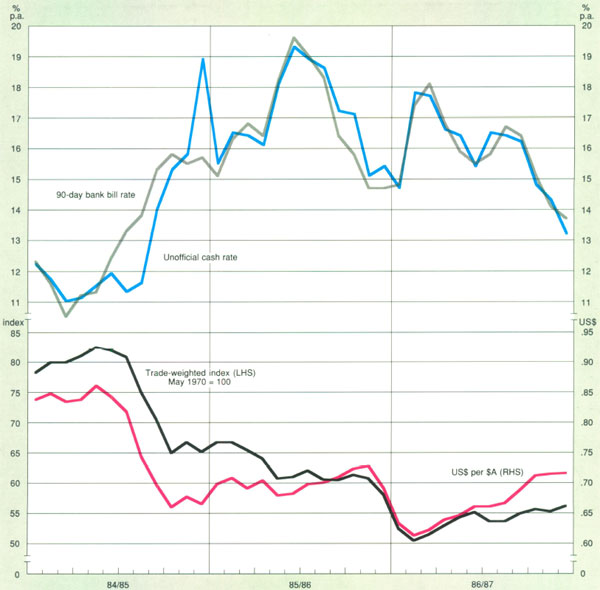

2 INTEREST RATES AND EXCHANGE RATES

Other things being unchanged, these developments should provide a firmer underpinning for the exchange rate and improved prospects for sustainable reductions in interest rates. The climate for private investment, essential to further restructuring, should be improved. Also by year's end, there were signs that policies designed to encourage the movement of resources to expanding industries were beginning to bear fruit. The current account had improved; inflation, whilst still uncomfortably high, was falling; economic growth, though slow, and falls in real wages combined to prevent a major deterioration in the labour market.

At the same time there were some contrary considerations. Some of the boost to competitiveness from exchange rate depreciation had been eroded by our relatively high rate of price increases; the slight net appreciation of the Australian dollar over the year worked in the same direction. It had still to be demonstrated that changes to the wage-setting system would produce wage increases more closely aligned to productivity. Credit growth and inflation were falling only slowly. Overseas, the continuance of massive external imbalances among the major economic powers underlined the possibility of lower world growth and further instability in exchange markets.

Monetary policy in 1986/87

Monetary policy played a prominent role in the broad economic strategy of 1986/87. Monetary management through the domestic and foreign exchange markets sought to provide a generally stable financial environment while policies of more fundamental adjustment took hold. However, uncertainty and volatility in financial markets, particularly in the foreign exchange market, required more vigorous market operations by the Bank than has been usual or had been anticipated.

Monetary policy was tightened sharply on two occasions during 1986/87. In the period leading up to the Budget in August 1986, there was widespread uncertainty and lack of confidence. The exchange rate became the pressure point. A further major fall in the value of the Australian dollar at that time would have been unhelpful both practically and psychologically. The fall in the Australian dollar over the previous 18 months had provided an adequate basis for progressively correcting Australia's external accounts — if other policies were adjusted appropriately and business attitudes responded. Changes in other policy instruments were still to be announced; until they were, options were few. Monetary policy had to be tightened abruptly. The Bank took the unusual step of raising its rediscount rate ahead of the market to signal the policy tightening; market interest rates rose sharply; and large sales of foreign exchange were made out of official reserves.

These actions enabled the Budget to be brought down in a calmer atmosphere. Though the Budget's reception was initially lukewarm, over time confidence improved and it was possible to undo some of the additional monetary tightening.

The need for decisive action arose again in early 1987 when a re-alignment of European currencies and the consequent adjustment against the U.S. dollar sparked another sharp run on the Australian dollar. There had been no significant change in Australia's economic prospects, but investor assessment, particularly overseas, was that the Australian dollar would stay with the U.S. dollar. Once again, a firm response in domestic and foreign exchange markets calmed conditions but at the cost of another sizeable lift in domestic interest rates and use of official foreign exchange reserves.

Exchange market pressures were not always downward. Indeed, apart from the incidents mentioned above, the currency was stable or strengthening for much of the year. Over the final months of the year, the U.S. dollar was weak against most currencies, including the Australian dollar. This, together with an enhanced view overseas of investment in Australia, led to considerable buoyancy.

3 EXCHANGE RATES AND EXTERNAL DEBT

Over the year, the authorities thus had to deal with extremely strong pressures in the exchange market — in both directions. The response tended to be three-pronged: to varying extents pressure was absorbed in movements in interest rates, in the exchange rate and in the level of official reserves.

Reasonable stability in the exchange market had a high priority. However, the Bank's actions carried no suggestion that it believed it necessarily had superior judgement about what constituted a “correct” exchange rate. In general, a sharp fall in the exchange rate can be inflationary whilst a strongly rising exchange rate can erode competitiveness. Within those broad parameters (which will shift their location with changing conditions) it may be assumed that the market itself will establish prices at which trading can confidently be carried on. However, rumour and over-shooting, which are features of open financial markets, are factors that can significantly affect market conditions from time to time. It is against this background that the Bank seeks to be satisfied that emerging exchange rate movements are based on sound premises and reflect substantial volumes of trading.

Over the year as a whole, the exchange rate and official reserves both rose while interest rates, though high throughout, fell. These were net movements; there were very strong fluctuations in each item during the year; this is illustrated in the graph on page 17.

By most tests, monetary policy was very effective in the past year.

Money and credit aggregates grew more slowly in 1986/87 than in other recent years. These series continue to provide useful information about changes in monetary conditions but, in present conditions cannot be relied upon alone, or used as targets, in determining monetary policy.

Among other indicators, domestic demand was contained and net export production increased, contributing to the measurable progress made on the long task of correcting our balance of payments. This was achieved without the economy moving into recession. Inflation was still much too high by international comparisons but may have peaked.

Whilst of course, monetary policy was not the only factor in these developments it played an important part.

Towards the year's end, emphasis shifted further to fiscal and wages policy, allowing, it is hoped, some easing of the role of monetary policy in restraining consumption spending and, as those policy changes become effective, in lowering the “risk premium” in interest rates needed to reassure foreign investors. This would also be helpful to needed business investment. The scope to ease monetary policy, however, is constrained by the need to continue a restrictive setting of overall economic policy and regulated by the speed with which Australia's fundamental problems respond.

A major on-going task for monetary policy will be to maintain conditions conducive to the continuing inflow of foreign capital needed to offset the current account deficit and to retain the already large and growing stock of short-term funds invested in Australia.

The Bank and the financial system

The Reserve Bank, as central bank, has a close interest in the efficiency and stability of the financial system generally. As discussed later in this Report, it has special relationships with several groups of financial intermediaries.

Financial intermediation has been undergoing rapid change. The Bank holds regular meetings with representatives of institutional groups in order to keep abreast of developments. It publishes a wide range of data about the various groups obtained under the Financial Corporations Act.

During the year, further changes were made to the guidelines under which the authorised short-term money market dealers operate. Practices in the foreign exchange market are kept under review, particularly through the Foreign Exchange Market Consultative Group.

The Australian payments system has taken advantage of advances in technology, particularly in electronic funds transfers, in recent years. Australia is well to the fore in the application of this technology. The major banks have foreshadowed the introduction of an electronic Bank Interchange and Transfer System (BITS) for the secure and immediate transfer of high-value funds. This is expected to become operational in 1987/88 and will be available to both banks and other financial institutions. Direct participation of non-bank financial intermediaries in the domestic payments system was enhanced by the passage of the Cheques and Payments Orders Act in 1986. The Bank's participation in the development of the payments system includes Chairmanship of the Australian Payments System Council and membership of the Australian Clearing House Committee.

The Bank's accounts

The Bank's financial statements for 1986/87 are set out later in this Report.

The Bank's net operating earnings increased by about 30 per cent in 1986/87; this followed increases of around 40 per cent in 1985/86 and 90 per cent in 1984/85. Over recent years these increases have been substantially due to gains from the sale of foreign currency by the Bank at prices (in Australian dollar terms) higher than those at which it was acquired. The average price at which the Bank's present portfolio was acquired is close to the average market price and transactions at current prices would accrue little or no profits.

The volatility of exchange rates and security prices exposes the Bank to potentially large changes in the value of its assets. Provisions and reserves therefore are needed against possible falls in asset values and other contingencies.

Transfers to the Bank's reserves and provisions out of 1986/87 earnings totalled $801 million. After these transfers, and allocation to the Rural Credits Development Fund, the Bank's 1986/87 profits payable to the Commonwealth were $2,654 million.

The Treasurer, in accordance with the legislation providing for the termination of the Rural Credits Department, after consultation with the Board, has directed that $120 million of the capital and reserves of the Department be distributed — one half to the Reserve Bank Reserve Fund and one half to the Commonwealth. The amount of $120 million was found to be surplus to the requirements of the Rural Credits Department.