ISO 20022 Migration for the Australian Payments System –

Responses and Options Paper – September 2019

3. Message Design Enhancements

3.1 Summary of responses

3.1.1 Enhanced content

Respondents expressed strong support for including enhanced content in domestic ISO 20022 messages, in particular, payment purpose codes and identity information, along with increasing the remittance capacity of high value messages and using the Legal Entity Identifier (LEI) (Figure 4). Key reasons provided for supporting the implementation of enhanced content included improved risk management (particularly in terms of Anti-Money Laundering and Counter-Terrorism Financing (AML/CTF) compliance and sanctions screening) and the operational benefits attained through increased straight through processing from the use of structured data. Although the inclusion of International Bank Account Numbers (IBANs) received the least support, it was still supported by around 70 per cent of respondents. Responses suggested that, even if not mandated, it would be important that payment messages be able to include IBANs to enable interoperability with other jurisdictions using IBANs for account identification.

A related issue in defining ISO 20022 message enhancements is the extent to which particular fields in payment messages are able to, or required to, be populated using a specified data structure. This is discussed further in Box B.

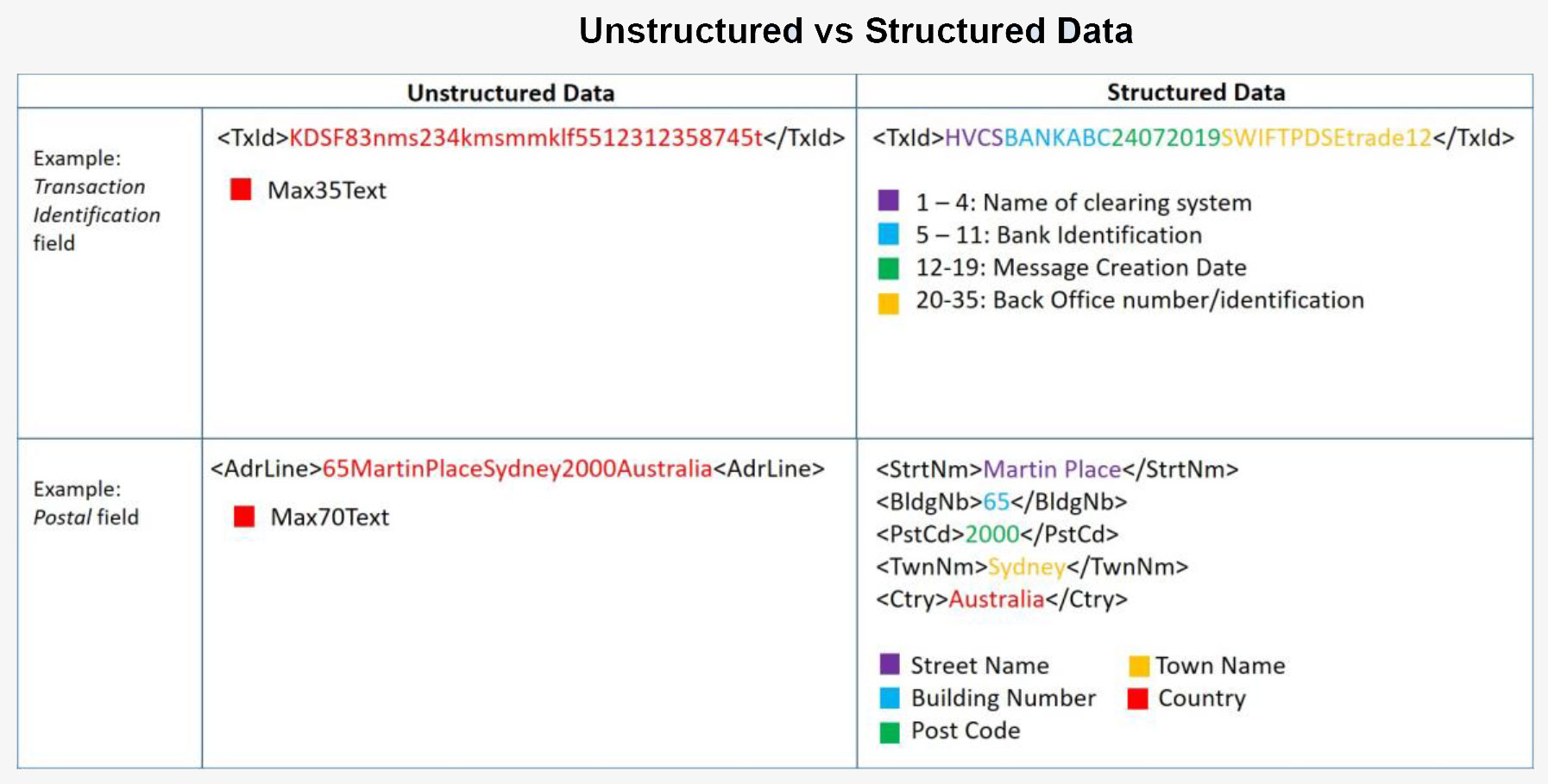

Box B: Structured data

As part of defining the ISO 20022 message standards, the industry will need to determine the extent to which structured or unstructured data is to be used within each message. Structured data means that data is logically populated in different elements in a pre-defined way to provide clarity and consistency in the way the content is carried (and processed). Unstructured data fields allow for the unrestricted entry of data within the boundaries of ISO 20022 data types. Figure 5 provides examples of unstructured and structured data.

Data can be structured in two ways:

- By defining how a specific ‘free text’ field is to be structured (see example of Transaction Identification field); and

- By requiring the use of specific fields (see example of Postal field).

There appears to be a strong case for fields to be structured (where possible) as there are some clear benefits that include: consistent formatting of data elements; minimisation of data misinterpretation; simplified data monitoring; improved reporting; and improved effectiveness of compliance screening. The use of structured data is consistent with global trends and CBPR+ guidelines and will be mandatory in some overseas payments jurisdictions.[9] The fields where the use of structured data is most suitable are the address, party identification, and remittance fields but the domestic implementation may choose to take a broader approach.

Consultation Questions

- Does your organisation have any views regarding the use of structured data in payments messaging?

3.1.2 Message harmonisation

Most respondents recognised the advantages that might accrue from aligning, to the extent possible, domestic ISO 20022 message usage guidelines across different clearing systems as well as with the message usage guidelines being used overseas. There was general agreement that the starting point for defining domestic credit message standards should be the internationally agreed HVPS+ guidelines for domestic real-time gross settlement (RTGS) systems (Figure 6). It was noted that the Australian domestic usage guidelines may need to deviate from HVPS+ but that any deviation should be kept to a minimum. Some respondents also noted the CBPR+ guidelines being developed for cross-border payments and indicated a desire to harmonise with those guidelines as well.

Some respondents expressed support for the development of a common domestic ISO 20022 message set across credit transfer clearing systems such as the HVCS and NPP. They felt this would allow for greater harmonisation, improved interoperability and choice, and would deliver operational resiliency benefits. Achievement of full interoperability of retail and high value payments systems via a common domestic credit message would not be without challenges. It may require NPPA's ISO 20022 domestic messaging and usage guidelines to be more closely aligned with global standards such as HVPS+ and CBPR+. Investigation would be required to determine the scope of technological build and implementation costs to upgrade participant back office systems and to develop industry agreed interoperability arrangements.

It was also noted that some major jurisdictions (including the United States, the Eurozone, and the United Kingdom) have recently agreed to adopt the 2019 version of the ISO 20022 standards for their upcoming implementations and that it would make sense if Australia adopted the same approach as part of its ISO 20022 migration.[10] These jurisdictions have also indicated their intention to upgrade to the latest ISO 20022 version by 2025 and to subsequently perform annual upgrades in November each year.[11]

As part of the migration project it would be worthwhile for the Australian payments community to consider and agree how the industry will manage ISO 20022 versions within and across payments systems in Australia on an ongoing basis. A new version of the ISO 20022 standard is generally released annually and this can be adopted at the discretion of individual payments systems. To the extent version management protocols can be agreed in advance, this would make investment planning for system upgrades more predictable and harmonisation with domestic and international systems more achievable.

3.2 Proposed message design enhancements

Based on the responses to the Issues Paper there appears to be general agreement that the ISO 20022 message usage guidelines developed for the Australian HVCS migration should:

- incorporate the mandatory use of payment purpose codes, enhanced identity information and additional remittance information

- allow for the use of LEIs and IBANs

- align message usage guidelines with HVPS+ and CBPR+ guidelines where possible

- use structured data in accordance with CBPR+ guidelines

- adopt the 2019 version of the ISO 20022 standards for the duration of the coexistence phase of the domestic migration project

- include arrangements for ongoing management of ISO 20022 versions to provide certainty and align with domestic and international usage.

A move to develop a common set of domestic messages using ISO 20022 for credit transfer systems in Australia is likely to be a long-term objective. Based on the responses received, most payments industry participants are already challenged with competing internal projects and harmonising to a common message standard in the short term would be an unnecessary expansion of scope that would put the proposed timeline at risk.

Consultation Questions

- Does your organisation support the proposed message design enhancements, as set out in Section 3.2? Please explain your view.

Footnotes

For example, as part of SWIFT's cross border ISO 20022 migration, structured agent identification data will be mandatory from the start of the coexistence phase if the originating cross-border message is in ISO 20022. [9]

These jurisdictions are using the Standards Release 2019 HVPS+ guidelines as a base for their implementations. [10]

This practice is in line with SWIFT's Harmonisation Charter: https://www.swift.com/standards/iso-20022-harmonisation-programme [11]