ISO 20022 Migration for the Australian Payments System –

Issues Paper –

April 2019

4. Strategic Issues – Payment System Design

- Download the complete Consultation Paper 1.60MB

- Download the Response Template 97KB

Consultation Paper

April 2019

4.1 Long-run payment system design considerations

A migration to the ISO 20022 standard presents an opportunity for the industry to consider the optimal long-run design of Australia's payments system. The changes required for an ISO 20022 migration can be considered and designed to align with the longer-term strategic direction desired by the industry. Accordingly, it is important the industry considers the strategic issues raised in this consultation in conjunction with long-run issues raised in the consultation on the APC's review of the Australian Payments Plan and any related work by the Australian Payments Network (AusPayNet).

In preliminary industry discussions on an ISO 20022 migration, some stakeholders have raised the question as to whether high value payments could be migrated to the NPP, thereby avoiding a separate upgrade of the HVPS to ISO 20022 messaging. The NPP is newly commissioned, operates on modern infrastructure and the message set is based on the ISO 20022 standard (Box B). For some participants, this may seem an attractive proposition, compared with the system upgrade work to move HVCS to ISO 20022. However, there are some significant issues that would need to be considered in determining the suitability of any potential migration of high value payments to the NPP. These include:

- Member participation in the NPP is relatively narrow. For example, direct participation in the SWIFT PDS (47 participants) is much larger than in the NPP (11 participants). Consequently, the overall quantum of work required for all HVCS participants to develop infrastructure to directly connect to the NPP would be significant.

- Under the RBA's existing ESA policy, ADIs must directly settle across their own ESA if their aggregate wholesale RITS RTGS transactions constitute 0.25 per cent or more of the total value of wholesale RITS RTGS transactions. This policy requirement, as well as NPP Australia's (NPPA) participant onboarding requirements, would need to be met in any proposed migration of high value payments to the NPP.

- Existing RITS functionality helps to facilitate efficient liquidity management processes for ESA holders for the settlement of their high value payments, including those processed through the SWIFT PDS. RITS allows transactions to be queued until sufficient settlement funds are available. It also provides other liquidity savings features such as transaction prioritisation and auto-offset.

- The settlement system used for NPP payments is the FSS. The FSS caters for fast, immediate settlement processing. It has no queuing, transaction management functionality, or liquidity saving features, which may make it unsuitable for the settlement of high value payments.

- It may be possible for the RBA to build functionality that allows payments sent from the NPP, or from other payment systems, to be settled in either RITS or the FSS (i.e. a choice in settlement method could be provided). Given the different levels of participation by institutions across payment systems, this would potentially be complex to implement.

- Existing cash market arrangements are based primarily on the processing arrangements and operating hours of Australia's high value systems, Austraclear and the SWIFT PDS. A careful analysis of the implications for the cash market from migrating high value payments to the NPP would be required to ensure that there are no adverse outcomes for the broader financial system, especially if operating hours were extended.

- For many HVCS members, large-scale systems and operational changes may be required to redevelop interactions between payment systems, back office and treasury systems, fraud, reporting and reconciliation systems as they may be heavily integrated in existing payment channels and business processes.

- A major advantage of maintaining two or more separate credit transfer systems is that, in the event one of the systems becomes unavailable in a contingency scenario, payments can be redirected to a different system for processing. This mechanism has been successfully used by Australian institutions during a number of contingency events to maintain customer service availability. The potential resiliency benefits for some participants of being able to route payments through a different clearing system, which is also ISO 20022 compatible, in a contingency would be lost if NPP and HVCS were merged.

Accordingly, migrating high value payments to the NPP in place of migrating SWIFT PDS to ISO 20022 messaging is not a simple or straightforward option. While some HVCS payments have already, or will in the future, migrate to the NPP, this does not necessarily obviate the need to maintain a distinct HVPS. With two distinct systems, there would be potential merit in developing contingency capability to allow payments to be sent through either the NPP or SWIFT PDS to allow critical payments to flow in the event that one system becomes unavailable.

Industry stakeholders should also consider the long-term future of the DE clearing system in relation to the ISO 20022 migration. The cost and effort of migrating legacy DE systems to ISO 20022 messaging would be large and the industry may not consider this migration to be worthwhile. As with the HVCS, some credit payments currently cleared through DE are candidates to migrate to the NPP. With the proposed development of an NPP Consent and Mandate Service, debit payments would also be candidates to migrate to the NPP. These developments may lead to the decline in use of DE to the extent that the industry may consider whether to continue the ongoing support of this clearing system.

Similarly, with the decline in cheque use in Australia, the industry is likely to consider the length of its ongoing support of this clearing stream and therefore may not consider a migration to ISO 20022 worthwhile.

Box B: The NPP

The NPP facilitates the 24/7 real-time clearing of consumer and business payments, with settlement occurring in the RBA's FSS. There are currently more than 75 banks, credit unions and building societies that have rolled out real-time payments services to their customers, of which 11 participants undertake settlement in FSS. The NPP utilises ISO 20022 messaging for the clearing and settlement of payments. Figure 2 shows the order of message flows in the NPP.

NPP payments are generally associated with an overlay service, which can range from arrangements that set service standards to more complex solutions that implement new flows and payment types between participants. The first overlay service is Osko by BPAY, which is a payment option available through participating digital banking channels, such as mobile applications and online banking, on a 24/7 basis that enables funds and information to be rapidly transferred and made available to recipients.

Consultation Questions

Q10. Do you agree with the view that it is appropriate to maintain a dedicated HVPS alongside other payment systems, including the NPP? If no, please explain your views.

Q11 a) Does your organisation have any other views or preferences on how the long-term design of the Australian payments system should evolve?

Q11 b) If yes, how does choice of settlement method and system resiliency factor into this view?

Q11 c) From your organisation's perspective, what other long-term design considerations should be factored into this migration project? Please frame your response from a strategic standpoint rather than any focus on short-term challenges or required investment.

4.2 RTGS message exchange models

The move to ISO 20022 message format standards internationally has also coincided with changes in how some RTGS operators propose to receive and process message content in their HVPSs. As is the case with other central banks, the RBA is considering the appropriate message and network exchange model to adopt for the processing of high value payments as part of the ISO 20022 migration project.

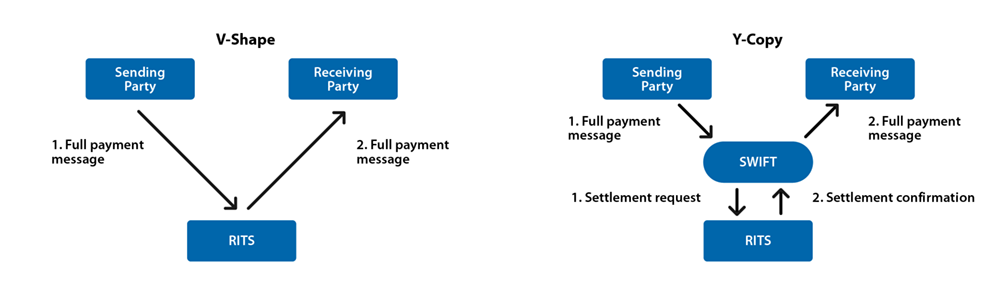

The majority of HVPSs around the world, including the SWIFT PDS, use SWIFT's Y-Copy messaging service (Figure 3). The Y-Copy service involves the sending party (the HVCS/RITS member) sending the full payment clearing message to the SWIFT network, which then extracts relevant interbank settlement details to send to RITS for settlement. Upon settlement, RITS sends a confirmation to the SWIFT network which then releases the full payment message (including the settlement confirmation) to the receiving party (another HVCS/RITS member) while also notifying the sending party of the successful settlement.

Under the Y-Copy service, RITS receives no information about the sending or receiving customer. In addition, message routing and security are handled by SWIFT, as the network operator, at each transit point. From a contingency perspective, it is possible for the Y-Copy service to support continuation of clearings when RITS is unavailable.

An alternative option is a V-Shape model. The V-Shape model involves the sending party sending the full payment clearing message to RITS for settlement. Upon settlement, RITS sends the full payment message (including the settlement confirmation) to the receiving party. Under this model, the full payment message, including customer information, is received by RITS.

A feature of the V-Shape model is that it does not necessarily require SWIFT to operate the network and the system may even become ‘network agnostic’. This could have some advantages in terms of resiliency because industry participants could potentially connect to more than one network to clear and settle payments for a particular payment system. This could provide contingency options in the event of one network, or the RITS interface to that network, being unavailable as payments could be routed through the other network. Support of multiple networks may also increase competition between network providers and therefore reduce prices.

However, allowing clearing systems to use multiple networks to connect to RITS would introduce additional complexity, and therefore cost, as different network protocols, security protocols and gateways would need to be supported. Other potential implications of adopting a V-Shape architecture may include changes for how end-point security and message routing is managed and a need for additional transaction screening.

In each model, interbank settlement in RITS would occur before the completion of the payments clearing.

View enlargement

View enlargement

Consultation Questions

Q12. If a separate high value clearing system is maintained for the ISO 20022 payments migration, what is your organisation's preference on the RTGS messaging model (i.e. Y-Copy or V-Shape) that should be adopted? Please explain your views.