Reserve Bank of Australia Annual Report – 2021Earnings, Distribution and Capital

In 2020/21, the Bank recorded an accounting loss of $4.3 billion, as unrealised valuation losses exceeded the sum of other components of profit. Despite the accounting loss, earnings of $3.9 billion were still available for distribution. This was because, when determining the amount available for distribution under the Reserve Bank Act 1959, unrealised valuation losses are offset against previously retained unrealised valuation gains. A sum of $1.2 billion was transferred to the Reserve Bank Reserve Fund (RBRF), consistent with the Reserve Bank Board's target for this reserve; $2.7 billion will be paid as a dividend to the Australian Government in September.

While the Reserve Bank earns a profit in most years, it also holds capital and reserves to cover potential financial losses when they occur. The framework for assessing the Bank's target level of capital was reviewed and updated during 2020/21, in response to the significant change in the size and structure of the Bank's balance sheet. The Board views the Bank's capital as appropriate given the risks arising from its assets and liabilities.

The Reserve Bank's earnings

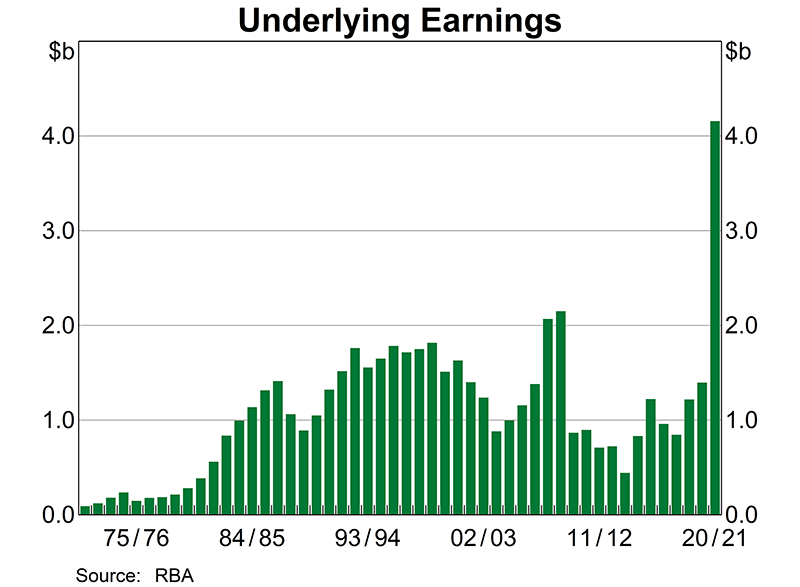

The Reserve Bank's earnings come from two sources: underlying earnings, including net interest and fee income, less operating costs; and valuation gains or losses. Net interest income arises from the Bank earning interest on almost all of its assets, albeit currently at low rates, while paying no interest on a large portion of its liabilities – namely, banknotes on issue, and capital and reserves. Moreover, Exchange Settlement (ES) balances, which have grown significantly over the past year as a result of the Bank's policy actions, are also currently paid a zero interest rate. Fees paid by authorised deposit-taking institutions in relation to the Committed Liquidity Facility also contribute to underlying earnings.

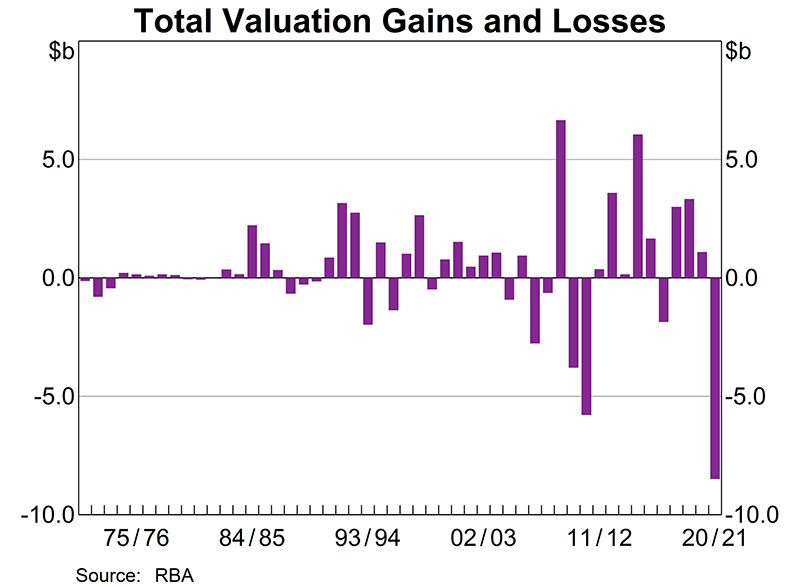

Valuation gains and losses result from fluctuations in the value of the Reserve Bank's assets because of movements in exchange rates or changes in the market yields on securities held outright. A depreciation of the Australian dollar or a decline in market yields results in valuation gains. Conversely, an appreciation of the Australian dollar or a rise in market yields leads to valuation losses. These gains and losses are realised only when the underlying asset is sold or matures. Valuation gains and losses are volatile, as both exchange rates and market interest rates can fluctuate in wide ranges over time. Market risk is managed by the Bank within strict parameters, although it is not completely eliminated given the policy purposes for which the Bank's assets are held.

Management of the Bank's assets is discussed in the chapter on ‘Operations in Financial Markets’; the associated risks are outlined in the chapter on ‘Risk Management’.

The Reserve Bank reports net profit in accordance with Australian Accounting Standards, while the distribution of profits is determined by section 30 of the Reserve Bank Act. In terms of the Act, net profit is dealt with in the following way:

- Unrealised gains (or losses) are not available for distribution and are transferred to (absorbed by) the unrealised profits reserve. The remainder of net profit after this transfer is available for distribution.

- The Treasurer determines, after consulting the Reserve Bank Board, any amounts to be placed from distributable earnings to the credit of the RBRF, the Bank's general reserve.

- The remainder of distributable earnings is payable as a dividend to the Commonwealth.

In 2020/21, the Reserve Bank recorded an accounting loss of $4.3 billion, comprising:

- Underlying earnings of $4.2 billion, an increase of $2.8 billion from the previous year. This increase reflects interest earnings on Australian government bonds purchased as part of the Bank's policy responses to the COVID-19 pandemic, including under the bond purchase program and to support the three-year yield target. At the same time, the corresponding liability, ES balances, were paid a zero interest rate since November 2020.

- Unrealised valuation losses of $8.2 billion, from:

- the appreciation of the Australian dollar over the year ($3.5 billion loss)

- a rise in bond yields in Australia and abroad ($2.0 billion loss)

- the unwinding of premiums on domestic government bonds that were purchased at a higher price than their face value (due to their coupon rates being greater than the market yields at the time) ($2.7 billion loss). These premiums are unwound on a straight-line basis and recorded as unrealised valuation losses each day, and realised upon sale or maturity of the bond.

- Realised valuation losses of $0.2 billion, from maturities of Australian government bonds that had been purchased at a premium, partly offset by gains realised on sales of foreign exchange in the normal course of managing the portfolio of foreign reserves. Taking account of coupon payments received on while these bonds were held, these holdings were profitable for the Bank.

Despite the accounting loss in 2020/21, earnings of $3.9 billion were still available for distribution, as unrealised losses of $8.2 billion were absorbed by the unrealised profits reserve in accordance with the Reserve Bank Act (explained above).

Capital, reserves and distribution

The Reserve Bank maintains capital and reserves for the risks on its balance sheet. These include the RBRF, which is the Bank's general reserve established under the Reserve Bank Act. The RBRF is funded from transfers from earnings available for distribution.

The Reserve Bank Board has for many years had a policy of aiming to hold sufficient funds in the RBRF to absorb losses that might reasonably be anticipated from time to time. The Board has a framework that assigns capital to various risks on the Bank's balance sheet, including credit risk and market risk. It calculates a target balance for the RBRF based on an assessment of these risks. This target balance is used as an input into the Board's advice to the Treasurer about dividend payments from distributable earnings. It is not a minimum level of capital that needs to be maintained at all times. At the end of the previous financial year, the target balance of the RBRF was $12.6 billion and the actual balance was $14.1 billion.

The capital framework is reassessed over time to take account of the changing risk environment or material changes in the composition of the Bank's balance sheet, as was the case in 2020/21. It was appropriate to do so given the significant changes in the size and structure of the Bank's balance sheet, the changes in the operation of monetary policy and the changed nature of the risks.

The Reserve Bank's existing capital framework accounts for credit risk and market risk:

- The Bank has no history of loss from credit risk and the capital held against credit risk is very small. This reflects the high quality of the Bank's assets, the soundness of the counterparties with which it deals, and the fact that repurchase agreements and foreign exchange swaps are highly collateralised. The expansion of the Bank's balance sheet over the past year has not materially changed the assessment of credit risk.

- The largest potential for loss from the Bank's assets comes from market risk, comprising foreign

exchange and interest rate risk. The capital assigned to each component of market risk is based on

the Bank's own experience as well as stress tests of the balance sheet, which incorporate

significant adverse movements in exchange rates and interest rates drawn from historical experience.

- For foreign exchange risk, the stress scenario used is a 25 per cent appreciation of the Australian dollar in a given year. As at 30 June 2021, the target level of capital for exchange rate risk was $12.8 billion, a little higher than a year earlier.

- For interest rate risk, the scenario that has been used for some years is a 200 basis point rise in interest rates across the whole yield curve. For the foreign portfolio, this results in a capital target of $0.6 billion, similar to that of 2019/20. For the domestic portfolio, the comparable figure is $27.4 billion, which is a very large increase from a year earlier. This increase reflects the significant expansion of the Bank's balance sheet.

Combining the capital calculations for credit risk, foreign exchange risk and interest rate risk generates an overall figure of $40.8 billion.

The Reserve Bank Board's recent review of the capital framework focused on interest rate risk for the domestic portfolio, particularly given that the government bonds purchased under the bond purchase program and to support the three-year yield target are intended to be held to maturity. For these bonds, any mark-to-market valuation losses that occur as yields increase will be offset at the time that the bonds mature at their face value. This means that fluctuations in yields alter the timing of any valuation gain or loss over time, but do not change the ultimate return the Bank will earn on these bonds. This would not be the case if the bonds were sold prior to maturity. Given the intention to hold these bonds to maturity, the financial risks are different from other bond holdings and the Board judged that this should be reflected in an alternative assessment of the risks associated with these bonds.

The Board also considered the financial risks arising from the mismatch between having fixed-rate assets (the purchased bonds and funds lent under the Term Funding Facility (TFF)) and floating rate liabilities (the additional balances in ES Accounts). The interest rate on ES balances moves with the cash rate target, meaning that the Bank's net interest earnings are now exposed to a rise in the ES rate. This is because a future increase in the cash rate would result in the Bank paying a higher rate on its liabilities, but it would still be earning the same fixed interest rate on its assets. In the past this earnings risk was very small, given the close matching of maturity of the Bank's domestic assets and liabilities. Hence, there was no capital assigned to these ‘earnings at risk’.

To assess this risk, the maximum annual decline in net interest earnings over coming years is calculated based on the projected balance sheet and financial market expectations for the cash rate. Market expectations for the cash rate have been used solely as an independent input, and should not be viewed as providing information on the Reserve Bank's own guidance for the future path of the cash rate. The maximum annual decline in earnings is in the next two to four years, after which the risks decline when the bonds purchased to support the three-year yield target mature and the funds lent under the TFF are repaid.

The capital calculation for these ‘earnings at risk’ is $2.0 billion. Combining this with the figures for credit risk, foreign exchange risk and interest rate risk on the foreign portfolio generates a total of $15.4 billion.

The Reserve Bank Board will continue to monitor the capital calculation based on interest rate risk on the domestic portfolio (assuming a 200 basis point rise in yields), as well as the earnings at risk on the domestic portfolio. In the interest of transparency, the Bank will continue to report both figures in the Annual Report.

The Board is mindful that valuation losses in any given year could be large enough to exceed the balance in the RBRF and result in a negative equity position. Such an outcome, if it were to occur for these reasons, would not affect the Reserve Bank's ability to operate effectively or perform any of its policy functions.

After consulting with the Board, the Treasurer determined that a sum of $1.2 billion be transferred from earnings available for distribution to the RBRF. This sum brings the balance in the RBRF to the Board's target of $15.4 billion. Following this transfer, a sum of $2.7 billion was payable as a dividend to the Commonwealth.

In addition to the RBRF, the Reserve Bank maintains a number of other financial reserves.

| 30 June 2021 | 30 June 2020 | |

|---|---|---|

| Reserves | ||

| Reserve Bank Reserve Fund | 15,366 | 14,119 |

| Unrealised profits reserve | 502 | 8,751 |

| Asset revaluation reserves | 6,753 | 7,335 |

| Superannuation reserve | 344 | 87 |

| Capital | 40 | 40 |

| Total | 23,005 | 30,332 |

|

Source: RBA |

||

The balance of the unrealised profits reserve stood at $0.5 billion at 30 June 2021, a decline of $8.2 billion from the previous year. The balance of this reserve is available either to absorb future valuation losses or to be distributed over time as the gains become realised when relevant assets are sold.

Asset revaluation reserves are held for non-traded assets, such as gold holdings and property. Balances in these reserves represent the difference between the market value of these assets and the cost at which they were acquired. The total balance for these reserves was $6.8 billion at 30 June 2021, $0.6 billion lower than in the previous financial year, largely reflecting a decrease in the Australian dollar value of the Reserve Bank's holdings of gold.

Details of the composition and distribution of the Reserve Bank's profits are contained in the table at the end of this chapter.

The Financial Statements (and accompanying Notes to the Financial Statements) for the 2020/21 financial year were prepared in accordance with Australian Accounting Standards, consistent with the Finance Reporting Rule issued under the Public Governance, Performance and Accountability Act 2013.

| Composition of Profits(a) | Distribution of Profits | Payments to Government | |||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|

| Transfer to/from(–) | |||||||||||

| Underlying earnings | Realised gains and losses (–)(b) | Unrealised gains and losses (–) | Accounting profit or loss (–) | Unrealised profits reserves | Asset revaluation reserves | Reserve Bank Reserve Fund | Dividend payable | Paymentfrom previous year's profit | Payment delayed from previous year | Total payment | |

| 1997/98 | 1,750 | 966 | 1,687 | 4,403 | 1,687 | −558 | 548 | 2,726 | 1,700 | – | 1,700 |

| 1998/99 | 1,816 | 2,283 | −2,773 | 1,326 | −2,349 | −1 | – | 3,676 | 2,726 | – | 2,726 |

| 1999/00 | 1,511 | −708 | 1,489 | 2,292 | 1,489 | – | – | 803 | 3,000 | – | 3,000 |

| 2000/01 | 1,629 | 1,200 | 320 | 3,149 | 320 | −5 | – | 2,834 | 803 | 676 | 1,479 |

| 2001/02 | 1,400 | 479 | −11 | 1,868 | −11 | −10 | – | 1,889 | 2,834 | – | 2,834 |

| 2002/03 | 1,238 | 1,157 | −222 | 2,173 | −222 | −2 | 133 | 2,264 | 1,889 | – | 1,889 |

| 2003/04 | 882 | −188 | 1,261 | 1,955 | 1,261 | – | – | 694 | 1,300 | – | 1,300 |

| 2004/05 | 997 | 366 | −1,289 | 74 | −1,289 | – | – | 1,363 | 374 | 964 | 1,338 |

| 2005/06 | 1,156 | 4 | 933 | 2,093 | 933 | −17 | – | 1,177 | 1,063 | 320 | 1,383 |

| 2006/07 | 1,381 | 72 | −2,846 | −1,393 | −2,475 | −3 | – | 1,085 | 1,177 | 300 | 1,477 |

| 2007/08 | 2,068 | 614 | −1,252 | 1,430 | 27 | – | – | 1,403 | 1,085 | – | 1,085 |

| 2008/09 | 2,150 | 4,404 | 2,252 | 8,806 | 2,252 | – | 577 | 5,977 | 1,403 | – | 1,403 |

| 2009/10 | 866 | −128 | −3,666 | −2,928 | −2,248 | – | −680 | – | 5,227 | – | 5,227 |

| 2010/11 | 897 | −1,135 | −4,651 | −4,889 | −23 | – | −4,866 | – | – | 750 | 750 |

| 2011/12 | 710 | 405 | −39 | 1,076 | −20 | – | 596 | 500 | – | – | – |

| 2012/13 | 723 | −135 | 3,725 | 4,313 | 3,725 | – | 588 | – | 500 | – | 500 |

| 2013/14 | 9,242(c) | 790 | −640 | 9,392 | −640 | −3 | 8,800 | 1,235 | – | – | – |

| 2014/15 | 832 | 2,622 | 3,434 | 6,888 | 3,434 | – | 1,570 | 1,884 | 618 | – | 618 |

| 2015/16 | 1,223 | 3,389 | −1,729 | 2,883 | −1,729 | – | 1,390 | 3,222 | 1,884 | 618 | 2,501 |

| 2016/17 | 960 | 322 | −2,179 | −897 | −2,179 | −4 | – | 1,286 | 3,222 | – | 3,222 |

| 2017/18 | 845 | −176 | 3,178 | 3,847 | 3,178 | – | – | 669 | 1,066 | – | 1,066 |

| 2018/19 | 1,167 | 412 | 2,970 | 4,549 | 2,970 | −106 | – | 1,685 | 669 | 220 | 889 |

| 2019/20 | 1,399 | 1,168 | −79 | 2,488 | −79 | – | – | 2,567 | 1,685 | – | 1,685 |

| 2020/21 | 4,157 | −240 | −8,249 | −4,332 | −8,249 | −1 | 1,247 | 2,671 | 2,567 | – | 2,567 |

|

(a) As originally published Source: RBA |

|||||||||||