Reserve Bank of Australia Annual Report – 2018 Banking and Payment Services

The Reserve Bank provides banking and payment services to support the efficient and stable functioning of the Australian financial system. The Bank is currently engaged in projects to renovate and strengthen its banking and settlement capabilities and operate new infrastructure to support real-time payments by households and businesses on a 24/7 basis. This will enable the Bank to continue to meet the banking and payment needs of its government and agency customers and, in turn, the Australian public.

Banking

The Reserve Bank's banking function provides services in two broad groups: central banking services and transactional banking services. Both are provided with the objective of delivering secure and efficient arrangements to meet the banking and payment needs of the Australian Government and its agencies. In addition, the Bank provides banking and registry services to a number of overseas central banks and official institutions.

The key aspect of the Reserve Bank's central banking services is the role it plays as banker to the Australian Government. Among other things, this requires the Bank to manage the consolidation of all Australian Government agency account balances, irrespective of the financial institution that provides transactional banking services to each Australian Government agency. These balances are transferred at the end of the business day into a group of accounts known as the Official Public Accounts (OPA) Group, which is where the Commonwealth's overnight at call cash balances are held. Daily payment instructions from the Department of Finance are then processed to move funds from the OPA to agency bank accounts to meet agency payment obligations. The Bank also provides the government with a term-deposit facility for investment of its cash holdings, as well as a very limited short-term overdraft facility to cater for occasions when there is unexpected demand for government cash balances. While the Bank manages the consolidation of the government's accounts, the Australian Office of Financial Management has responsibility for ensuring there are sufficient cash balances in the OPA to meet the government's day-to-day spending commitments and for investing excess funds in approved investments, including term deposits with the Bank.

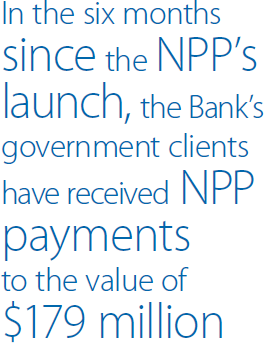

The transactional banking services offered by the Reserve Bank have evolved rapidly over recent years as its government agency customers look to embrace new technology to deliver convenient, secure, reliable and cost-effective payment options to the public. The public launch of the New Payments Platform (NPP) in February 2018 was an important milestone in this evolution. The NPP allows fast, versatile and data-rich payments to be made 24/7. In the six months since the NPP's launch, the Bank's government clients have received NPP payments to the value of $179 million, primarily from individuals and businesses to pay tax liabilities. The Bank is working with government agencies, such as the Department of Human Services and the Australian Taxation Office (ATO), to ensure they are able to fully utilise the new payments technology, including via future planned overlay services. The Bank expects that the NPP will affect volumes for its more traditional payment and collection services in coming years.

The Reserve Bank also continues to provide a number of other channels to make payments from government agencies to recipients' accounts. In 2017/18, the Bank processed around 312 million domestic and 1.1 million international payments, totalling $534 billion and $11.6 billion respectively, for government agencies. Most of these payments were direct entry payments made on behalf of the Department of Human Services. The Australian Government also makes payments by the real-time gross settlement (RTGS) system, cheque, BPAY and prepaid cards. After declining over recent years, cheque payment volumes were steady in 2017/18.

In addition to payments, the Reserve Bank provides government agency customers such as the ATO with access to a number of services through which they can collect monies owed from both domestic and international payers. These include direct entry, RTGS, BPAY, cheque, eftpos, cash, and card-based services via the internet and phone. The Bank processed 36 million collections-related transactions for the Australian Government in 2017/18, amounting to $509 billion. Agencies continue to actively encourage customers to use lower-cost electronic payment options, with cheque and cash payments declining by 17 per cent to $4.8 million and electronic payments representing 98 per cent of all collections-related transactions in 2017/18.

The provision of transactional banking services is consistent with the Reserve Bank's responsibilities under the Reserve Bank Act 1959, which requires the Bank to provide these services to the Australian Government if so required. The Bank provides transactional banking services to over 90 Australian Government agencies. A key difference between the Bank's central banking and transactional banking services is that the latter are offered in line with the Australian Government's competitive neutrality guidelines. To deliver the services, the Bank competes with commercial financial institutions, in most instances bidding for business via tenders conducted by the agencies themselves. The Bank must also cost and price the services separately from its other activities, including central banking services, and meet a prescribed minimum rate of return.

Pro forma business accounts for transactional banking are provided on page 128 of this report.

The Reserve Bank works closely with its transactional banking customers, the Australian Government and the payments industry more broadly to ensure that its customers have access to the services which meet their needs and those of the public. For some services, the Bank combines its specialist knowledge of the government sector with specific services and products from commercial providers to meet the government's banking needs. In 2017/18, the Bank explored new options for collecting online payments. The Bank will continue to make use of combined service arrangements with commercial providers as the government's banking needs evolve.

Registry services are also provided by the Reserve Bank to supranational organisations issuing Australian dollar-denominated securities. Eight organisations currently use these services, with this number having been relatively steady over recent years.

The Reserve Bank has undertaken a significant program of work to upgrade its banking systems since 2012, moving them to a more modern programming language and architecture, and re-engineering a number of related business processes. Further milestones in the program were achieved during 2017/18, with work on renovating the systems used to process most government payments and collections almost complete. The Bank has also made good progress with the project to upgrade the Bank's account maintenance system, with the first phase completed. This program of work is on schedule to be completed during the September quarter 2019.

Since the launch of the NPP, the Reserve Bank has continued to develop further capabilities that will assist in providing more reliable, cost-effective, faster and better-integrated services to expand the usage of the NPP. As part of this work, an Application Programming Interface (API) will be introduced by the end of 2018 to facilitate open, secure and automated communications between the Bank and its agency customers.

After-tax earnings from the Reserve Bank's transactional banking services were $1.5 million in 2017/18, $1.9 million lower than in the previous year. The fall was due largely to higher project costs associated with systems development and service improvements combined with reduced interest income.

Settlement Services

The Reserve Bank owns and operates the Reserve Bank Information and Transfer System (RITS), which is used by banks and other approved institutions to settle their payment obligations. Settlement in RITS is effected across Exchange Settlement Accounts (ESAs) held with the Reserve Bank, and is final and irrevocable. Around 90 per cent of the value of payments exchanged between financial institutions in Australia is settled in RITS individually on a real-time gross settlement (RTGS) basis. This includes high-value customer, corporate and institutional payments, wholesale debt and money market transactions and the Australian dollar legs of foreign exchange transactions. By providing a mechanism for RTGS, RITS eliminates the settlement risk that would otherwise arise between participants in high-value payment, clearing and securities settlement systems. On average, 47,600 RTGS transactions worth $182 billion were settled in RITS each day in 2017/18. In recent years, the value of transactions has increased at a lower rate than the volume of transactions. In addition, RITS provides deferred net settlement services for low-value retail payment systems, equity settlements and settlement of property-related transactions.

RITS also provides a real-time settlement service to support the operation of the NPP. The public launch of the NPP in February 2018 was the result of a large collaborative undertaking by payment service providers and the Reserve Bank. The key features of the NPP include: enabling users to make retail payments in real time; allowing more complete remittance information to be sent alongside the payment; enabling easy addressing of payments to payee accounts using simple identifiers (called PayIDs), such as email addresses, mobile phone numbers or ABNs; and facilitating the sending and receiving of payments outside normal business hours with 24/7 operation. To support innovation in the Australian payments system, the NPP is structured so as to allow the commercial development of new payment and related services using the capabilities of NPP's infrastructure. At the end of June 2018, more than 60 financial institutions offered NPP payments to their customers, with around 1.8 million registered PayIDs. Many of these institutions are smaller authorised deposit-taking institutions (ADIs) connecting via the services of an aggregator. The number of registered PayIDs is expected to grow significantly through 2018/19 as participants progress their NPP roll-out.

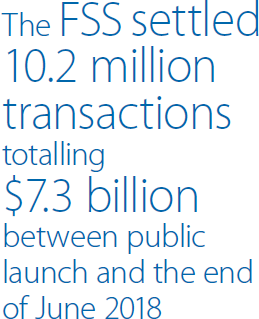

NPP transactions are settled in the RITS Fast Settlement Service (FSS). This is a new system within RITS designed to process and settle a high volume of transactions in real time, but without the transaction queuing and management capabilities provided by core RITS for the management of high-value transactions. The real-time settlement of NPP transactions via the FSS removes the credit risk that would otherwise exist if these transactions were settled on a deferred net basis as is currently done for other low-value payments. Transaction volumes settled via the FSS have grown steadily since launch, reaching over 100,000 transactions per day in June 2018, with an average transaction value of around $750. This amounted to a total of 10.2 million transactions with a total value of $7.3 billion settled via the FSS between public launch and the end of June 2018. To support the FSS, the hours of operation of the RITS Help Desk were extended to provide 24/7 technical assistance to members. Since its launch, the FSS has operated smoothly, with no major disruptions to operations.

While the introduction of the NPP has resulted in more low-value payments being settled in real time, the bulk of low-value payments continue to settle in RITS on a net basis. The average daily value of net settlements in RITS was around $12 billion in 2017/18. This includes obligations for payments exchanged through low-value clearing systems for cheques, debit and credit cards, BPAY and direct entry transactions. For these transactions, RITS combines multiple bilateral obligations submitted by members into a single net obligation for each member, which are then settled in RITS at predetermined times. During 2017/18, these low-value clearing arrangements accounted for a net daily average of $9.5 billion, of which around 85 per cent was intraday settlement of direct entry transactions. The substantial increase in the value of these low-value clearing arrangements over the past five years reflects a fragmentation of settlement arrangements, with the introduction of the five intraday settlement runs for direct entry and other new batch settlement arrangements, which supplement the long-established arrangement of a morning settlement session of net deferred obligations at around 9.00 am.

In the batch settlement arrangements, an approved administrator for each batch is responsible for calculating the net obligations of the batch participants and submitting those to RITS for settlement. The Clearing House Electronic Sub-register System (CHESS) batch, which effects settlement of payments arising from stock market transactions and is administered by ASX Settlement Pty Limited, averaged around $1 billion per day in 2017/18. The Mastercard batch, for settlement of domestic Mastercard obligations and administered by Mastercard International, averaged around $684 million over the same period. On 30 August 2017, a new eftpos batch, administered by eftpos Payments Australia Limited, went live for settlement of point-of-sale transactions processed through the eftpos system. Previously, these transactions had been settled the next day at around 9.00 am. The eftpos batch averaged around $284 million per day for the part of 2017/18 during which it was operational.

A batch feeder arrangement in RITS also supports the settlement of obligations arising from electronic property transactions processed by Property Exchange Australia Limited (PEXA). Timelines for migration to electronic e-conveyancing set by several state governments have contributed to ongoing strong growth in the number and value of property settlement batches processed in RITS, although off a low base. During 2017/18, the PEXA batch settlements averaged $668 million per day, more than double the figure for the previous year.

Reflecting the critical importance of RITS to the Australian financial system, the Reserve Bank conducts regular reviews of the resilience of RITS. An important part of this is the annual assessment of RITS against the Principles for Financial Market Infrastructures (PFMI) set by the Committee on Payments and Market Infrastructures (CPMI) and the International Organization of Securities Commissions (IOSCO). The May 2018 assessment of RITS against the PFMI concluded that RITS adhered to all relevant principles. It noted the existing high level of resilience of RITS, which includes replication of critical components and duplication of systems across two geographically separate sites, while also supporting the Bank's ongoing work to enhance resilience. Key examples of this work are an investigation into the potential use of non-similar technology to enhance recovery from cyber attacks, and the implementation of the remaining recommendations from the Bank's major reviews of security and resilience conducted through 2015 and 2016. The Bank has also commenced a multi-year project to upgrade the core network and application infrastructure of RITS.

At the end of June 2018, 58 RITS members were using their own ESA to settle their payment obligations. An additional 41 RITS members held a dormant ESA, settling all their obligations through another ESA holder acting as their settlement agent. There were also 65 RITS members that did not hold an ESA, but held RITS membership to satisfy requirements for participation in the Reserve Bank's open market operations.

Recent changes in bank regulations seeking to enhance competition and innovation in payment services have resulted in corresponding changes in the Reserve Bank's ESA Policy. In May 2018, the Banking Act 1959 was amended to allow all ADIs to use the term ‘bank’. The Australian Prudential Regulation Authority is also introducing a phased approach to authorising new ADIs, which allows new entrants to fast track a restricted ADI licence. As the bank designation is no longer a useful criteria for determining the appropriate type of RITS membership, the prior requirement for all banks to hold an ESA has been removed. The requirement for ADIs contributing more than 0.25 per cent of total wholesale RTGS value to hold and operate their own ESA remains. The new policy means that holding a dormant ESA has become optional for many existing ESA holders, although the Reserve Bank continues to offer the use of a dormant ESA to eligible banks and other payment service providers for contingency purposes.

The Reserve Bank offers accounts to other central banks and official institutions overseas to allow for settlement of certain Australian dollar payments, and provides safe custody services to these overseas agencies. The face value of securities held in custody by the Bank in this capacity was around $72 billion at the end of June 2018. The Bank also provides settlement services for banknote lodgements and withdrawals by commercial banks.