Speech Digital Transformation Lessons Learned

Today I am going to talk about the lessons the RBA has learned in delivering technology change over the past five years and our approach to our continuing digital transformation. Central to this discussion will be the answer to the question, ‘How do I deal with the problem of growing technology complexity?’ In answering this question, I will explore the causes of growing technology complexity in the RBA and discuss how we're addressing these with the three dimensions of our Digital Transformation: the first being our focus on the resilience of our platforms; the second our approach to ensuring a digitally skilled workforce; and the third our emphasis on building stronger collaboration between IT, our core business and policy areas and the broader industry we integrate into. Finally, I will highlight the competing tensions that accompany a Digital Transformation and how we're seeking to balance these to deliver a successful technology capability for the RBA and the Australian people.

As CIO, I'm often faced with the question, what role does technology play in the RBA? In answering this question, I note that technology supports many of the services the RBA delivers for the Australian people. The RBA is Australia's central bank, responsible for conducting monetary policy, maintaining a stable financial system and issuing the nation's Banknotes. The Bank also provides banking services to the Australian Government, being involved in the delivery and collection of payments for millions of Australian citizens in our role as banker to government and facilitator of payment settlements across the financial sector. All of these services are underpinned by digital platforms and the technology workforce that supports them.

Like other digitally reliant organisations, we are also faced with the risks associated with technology dependence. These include operational disruptions, cyber threats, the ongoing challenge of attracting and retaining a digitally skilled workforce, and the need to collaborate with others to constantly improve the services we offer.

Put simply, in today's world we cannot be an effective central bank supporting a successful economy, without having an effective technology capability. Today I want to share with you how we are approaching this compelling challenge.

The Growth of Complexity

With the digitalisation of banking and payments and the increasing shift of government towards delivering digital services to the public, the RBA finds itself at the intersection of digital disruption across a number of sectors in which we operate. Escalating cyber-security threats, FinTech innovation in banking services and crypto-currency-based alternatives to conventional payments all confront the sweet spot of central banking operations. To address these challenges, the RBA has had to modernise its technology platforms and deeply integrate them not just across the Bank, but with the broader industries we service.

By example, our New Payments Platform, and the Bank-managed Fast Settlement Service that underpins it, is integrated in real-time across the nation's banking sector. Similarly, our new core banking platform is plumbed via cloud-based API services into our government customers to enable real-time payments into citizen's accounts. The Bank's policy areas have developed new data platforms that consume massive data sets from across industry to assess credit risk and maintain stability across our markets. If you've ever wondered how digitally dependent and integrated the RBA is, let's agree to put that question to rest.

With the increasing digitalisation of the RBA's processes, there has come with it an increase in technology complexity. For the Bank, contributors to this complexity include:

- the digitalisation of platforms that underpin our role in banking, payments and market operations

- the complexity of integrating these platforms both within the Bank and into industry

- the increasing cyber and operational resilience needs of these platforms

- the demand for increased data analysis and insight to service our policy-setting responsibilities

These drivers contribute to a significant increase in the volume and variety of technologies managed by the RBA, each of which must be operated in highly available and secure environments.

The Arrival of Digital Transformation

In today's environment of interconnected payments, government banking and market data platforms, failure or compromise of our systems will have significant consequences. It's not surprising then that as the RBA we've continuously enhanced our governance, security and resilience, with an ongoing focus on quality and assurance.

Earlier this year, the Australian National Audit Office publicly noted the RBA as the most cyber-secure federal agency it has reviewed in recent years. Only a few years ago, the Australian Project Management Institute, awarded the RBA's IT Project Management Office the best PMO in the country.

As a Bank, we've delivered the New Payment Platform and its underpinning Fast Settlement Service. We've successfully completed our core banking modernisation program while decommissioning our legacy mainframe-based system. Over these past years, we've also released the next generation of polymer banknotes supported by integrated robotic and distribution systems.

I will put it to you that the challenge in the coming years is to go beyond only delivering new technologies and extend to how we digitally enable the entire RBA and its integration into the broader economy. It's no longer about transforming IT and is now about digitally transforming the Bank.

This transition from IT to Digital Transformation is a challenge many of you face. It is also how ‘digitally-native’ organisations already operate.

The RBA's Digital Transformation is underway and is characterised by three key shifts:

- Resilient Platforms – Our core services are built on resilient platforms that are deeply integrated with industry. These include our Payments, Banking, Financial Market Trading and Data platforms. They must be both operationally and cyber resilient.

- Digitally Skilled Workforce – Cross-functional digital skills demand Bank-wide talent, skills management and a constant focus on evolving and building key digital skills. For the RBA these especially include cyber, machine learning and data science capabilities.

- Collaborative Mindset – Digital capabilities do not respect organisational boundaries. For the RBA this means new collaboration between Business and IT functions – and critically collaboration with the industries we integrate with.

None of these elements are unique to the RBA. I see these digital transformations as necessary for the success of all organisations we interact with. I'd like to share our approach in delivering these shifts in the hope there may be some useful lessons for those of you on your own digital transformation journeys.

Resilient Platforms

The RBA delivers a range of technology-supported services. These have been underpinned by systems that have been developed over decades in some cases. Like some of the longer-lived organisations represented in this room, this is reflected in a diversity of technologies, ranging from mainframe-based applications to cloud-based services.

Over the past decade, the RBA has been progressively implementing our technology capabilities on digitised platforms – consolidating and modernising our systems to support our core functions: banking, payments, market operations and data-intensive policy areas.

The importance and interconnectedness of these digital platforms both within the Bank and into industry has grown over this period. In the past, the footprint of the RBA was felt largely through the effects of monetary policy decisions and its market operations. Today our digital platforms for payments and banking are now also on the critical path for daily operations within the broader economy.

For this reason, resilience features strongly in today's central banking parlance. The operational and cyber resilience of our digital platforms are key capabilities we constantly seek to improve. The effort of maintaining the continuous and secure operation of such deeply varied and interconnected systems can at times be a wicked problem.

By way of example, I'm sure many of you are familiar with the challenges presented by patching. Patches are improvements released by vendors that are often aimed at increasing the security of systems. Implementing timely patches reduces the likelihood that a security vulnerability in your technologies will be compromised by a malicious actor. Conversely, they can also confound our ability to maintain the ongoing operation of our key systems. Patches often fix vulnerabilities, though also commonly introduce incompatibilities and sometimes instability. Organisations, including the RBA, are often left weighing the risks of addressing security vulnerabilities with the risks of introducing operational instabilities.

One of the approaches that the RBA adopts include improving the visibility of resilience risks and our ability to address them by wrapping these platforms with common integration, security, infrastructure and, increasingly, cloud management platforms as well as creating a layer of oversight that allows for simplified management, operational availability and ongoing security. In many cases this oversight is informed by real-time analytics and now machine learning to allow us to understand and respond to risks immediately or predictively.

When the RBA experienced an operational incident last year our security monitoring detected increased vulnerability scanning on our internet presences almost immediately. It indicated to us that releasing updates to markets on operational matters provides information to malicious actors that is weaponised by machine learning systems almost immediately. Operational and cyber resilience risks go hand-in-hand and so must their controls.

Balancing these often-competing risks is a defining characteristic of the post-digital transformation environment into which many organisations are now emerging. In a world of increasing organisational dependency on digital platforms, the challenge of resilient digital platforms is one that all of you are facing in some way. You are either operating a digital platform that your stakeholders rely on to be secure and available, or you are reliant on one. I wonder where you sit on this spectrum.

A Digitally Skilled Workforce

The best platforms and intent to collaborate across organisation and industry will largely be ineffectual without a workforce equipped with the skills to meet the challenges presented by digital transformation. In the same way digital transformation transcends the limits of IT transformation, digital skills extend beyond technical competencies and encompass the range of people competencies and new ways of working that characterise today's successful organisation. These challenges are not entirely new however, and organisations that place emphasis on its people and their development are well positioned to meet them. I'd like to share with you some of the practices the RBA has applied to staff development to meet the challenge of attracting, developing and retaining a digitally skilled workforce.

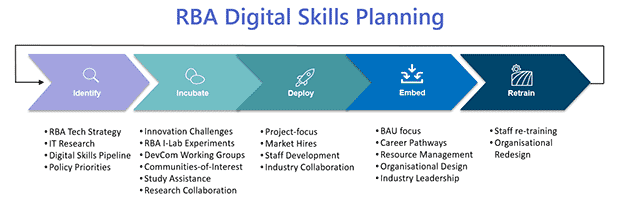

Most important to our approach to digital skills is planning. Without the variety of short-term incentives and remuneration benefits available to some commercial organisations, the RBA has instead relied on planning and a lifecycle-based approach to skills planning. We identify those skills the Bank needs to possess in the forward 3–5 year period and initiate an incubation process to identify staff with interests and competencies that can be developed into future required skills.

Source: RBA

Through stretch opportunities we develop a cohort of talent that are nurtured into developing key future skills and then look to embed these skills into the operations of the Bank. Reviewing the inventories of these skills allows us to ensure staff development plans are targeted towards required skills and, equally important, allows us to transition less demanded skills to ensure staff retain capabilities that benefit their own careers and the strategic needs of the Bank. Over the past decade this has allowed us to develop necessary skills and ensure those with these skills possess a deep understanding of the RBA and the contexts in which these skills are applied.

We have also strived to instil a positive digital workplace experience for our staff. This includes encouraging a culture of co-design, design thinking, staff engagement and customer satisfaction. As an IT function, we have found that when your staff, both within and outside of IT, are placed into a positive digital environment, they are better positioned to execute on the organisation's technology strategy while also fostering their uptake and development of key digital skills.

Without the skills needed to succeed in operating digital platforms and processes, any organisation, including the RBA, will fail to capitalise on the opportunities digitalisation provides them and, as importantly, risk being overwhelmed by the challenges they present. It has been our experience that we will suffer and lessen our quality outcomes if we do not plan and invest in the skills of our workforce. To succeed in digital transformation, we plan our investments, our project portfolios and our strategic partnerships. But as digitally maturing organisations do we invest enough time and effort into ensuring our people are equipped to allow us to address these challenges head on?

IT, Business and Industry Collaboration

A key element of a successful digital transformation is an organisation's ability to meaningfully collaborate across both its own operations and the broader ecosystem in which it operates. The RBA is no different and indeed the requirement to collaborate has deeply characterised the digital transformation the RBA has been undertaking for the past several years.

We've discussed that digital transformation is broader in scope than IT-centric transformation, with its focus being on organisational and ecosystem capabilities. The RBA has come from a place of strength in operational services to one where over the past decade it has had to develop further strengths in industry-facing program delivery. I've spoken about our recent collective industry experience in rolling out the New Payments Platform and the Bank's underpinning Fast Settlement Service. To illustrate another example of how much tighter collaboration is needed in a digital context, I would like to mention a specific case in which IT applied this ideology with an internal business partner, our Note Issue (NI) department, as we've met the challenge of releasing Australia's next generation of advanced polymer currency notes.

As you'd expect, our IT function had an enduring relationship with our Bank's Note Issue function. NI has served Australia well along with our partner, Note Printing Australia, for much of the innovative technology underpinning Australia's first and now second generation of advanced polymer notes. Several years ago, the Bank undertook the challenge of replacing our first generation of notes with a next generation sporting the cutting edge of advanced anti-counterfeit technologies. This is no simple challenge. It involves designing and manufacturing the notes with new techniques and, in Australia's case, implementing advanced robotic integration and replacing them with a new generation, all as seamlessly as possible. Merchants and banks are tightly involved, and ultimately everyone in Australia, including those abroad, needs to be educated on the design and security features of our notes.

To meet this challenge, we realised the need to refresh the way our IT and NI teams worked together. Starting with our people, we brought together staff from the business and IT to form a cross-skilled team which allowed us to collaborate within our organisation. Teams were co-located, trained in each other's processes and responsibilities, and focused on common objectives and milestones. Over time, and to go beyond mere operational collaboration, we developed joint engagement opportunities, including shared innovation activities on machine learning with other leading central banks, which allowed us to innovate and now apply advanced machine learning techniques to tackle fraud risks in Banknote processing. The joint engagement outcomes of this collaboration priority speak for themselves. We continue to have arguably the most advanced notes in the world as we near the completion of a massive generational update of banknotes across the nation, and importantly workforce engagement across our joint teams is at record levels. I'd put it to you the two are related: a poor collaboration across IT and business will never achieve the ambition demanded by an organisation that must collaborate deeply with industry.

Collaboration across IT and the business is by no means constrained by organisational boundaries in a digitally transformed world. Effective digital transformation creates platforms and dependencies that are not confined in their reach to any one organisation, but across the industries in which they participate. I've already spoken of the Fast Settlement Service and New Payments Platform initiative across the financial sector requiring deep collaboration across all major banking sector participants.

Our experience at the RBA has been that success in digital transformation demands active participation in these kind of collaborative initiatives. A way of measuring the health of a digitally capable organisation is by assessing how much it gives and takes from these collaborations. A key question to ask ourselves then is are we actively initiating partnerships within our organisations and the broader industries we participate in?

Balancing the Competing Tensions of Digital Transformation

We've now discussed three key elements of a successful digital transformation – establishing operational and cyber resilient digital platforms, maintaining a digitally skilled workforce, and establishing deep collaboration across business, IT and industry.

I'd like to conclude by sharing one observation we've experienced in navigating our digital transformation at the RBA. This is the need to balance the often-competing tensions involved in achieving digital transformation.

What do I mean by competing tensions? As digital challenges arise and need to be addressed, an emerging trend has been the competing demands that come with achieving improvements in key dimensions of digital performance. An example of this we spoke of earlier was the sometimes-conflicting needs of ensuring the stability of systems through tightly controlling their changes while also maintaining their security through regular patching.

The tensions of sustaining digital transformation are everywhere. The same digital platforms that support your organisation and which your partners are increasingly integrated into demand ongoing innovation and flexibility to address changing demands. The pace of delivery of constant change into platforms is leading to subsequent changes in conventional practices for maintaining their operation. Development and operations, once tightly separated are now increasingly merged with DevOps, and new combinations of so called ‘BizDevOps’ and ‘SecDevOps’ represent further compressions of system lifecycles to encourage faster delivery times and organisational agility. The pressures for agility and innovation on digital platforms often seems to characterise the experience of organisations like the RBA that are undertaking digital transformation. Balancing the often-competing tensions of these demands for agility, innovation, stability and security seem to be the diet on which CIOs are weaned.

In many cases, progress in one dimension of digital transformation requires careful consideration of its impact in another. Failure to manage this tension can result in significant failure, such as a failure to deliver highly available and secure services, or a failure to keep up with market innovation and customer expectations and demands. I would put it to you that unless you consciously seek to connect the outcomes of your paths of digital transformation, they risk confounding each other and limiting your overall progress. Achieving innovation and agility with a mind to doing so securely, and aiming to deliver change while being mindful of the need to retain stability will allow you to move your digital transformation agenda forward. It was a not a co-incidence we targeted innovative machine learning experimentation in our note issuing collaboration into areas that would increase the security of our processes. By connecting the dots on the sometimes-competing streams of digital transformation, we managed to balance tensions and achieve strong outcomes on all fronts. It's now a question I often ask myself: how do I progress transformation by concurrently addressing multiple requirements? How are you connecting the dots for your digital transformation?

Looking Ahead

Going forwards, it is imperative that we consider digital transformation and the role it will play in aligning our organisation with the world it now operates in. As our technology platforms are increasingly agile to fast-evolving requirements and integrated across industries with interwoven networks, the importance of resilience, collaboration and the skills we leverage to do so will continue to grow. These are not outcomes to be achieved in isolation but require considered alignment and investment of time and effort. A unified approach to digital transformation ensures that conflicting objectives do not hinder the development of critical digital competencies.

Digital transformation is a significant undertaking facing all organisations. It's a transformation that is not simply tackled and not all organisations will emerge successfully on the other side. I hope today's discussion has shed light on the approach the RBA has taken to making this transition and contributes in some way to your own success as you undertake your own digital transformations.

Endnotes

I would like to thank Lucas Wong, Bonney Joseph, Lily Yang and Charmaine Batulan for helpful input. [*]